High Yield: Odfjell, Noble, Murphy, Borr and Kosmos

Oil & gas credit perspectives on relative value including thoughts on Norwegian semisubs, jackups, and deepwater E&P

This note assesses recent developments in offshore drilling and select E&P credits, focusing on contract quality, capital intensity and relative value in high-yield debt. Noble’s Norway entry introduces execution risk, while Odfjell remains well positioned with a fully contracted, premium fleet. Jackup markets have stabilized, creating selective secured-bond value. Among E&Ps, Murphy offers balance-sheet resilience and exploration optionality, while Kosmos remains distressed but highly leveraged to improving commodity prices

Odfjell and Noble: Noble announced entry into the Norwegian semisub market with a 3-year AkerBP contract for the GreatWhite at an estimated ~$430k dayrate. The rig will require at least ~$160mm of upgrades to meet Norwegian standards, reflecting its unique position as a Moss CS60 design that is technically similar to Norway-eligible semisubs but was not originally built for NCS operations and thus requiring meaning capex spend. While expensive, Noble is buying much stronger utilization visibility on GreatWhite with this unique transaction. As detailed in Outlook 2025: Semisubs, being eligible to work in Norway is important for harsh environment rigs.

Noble’s Ocean GreatWhite is currently stacked in Norway with limited near-term opportunities amid lower oil prices and continued weakness in the UK North Sea due to unfavorable tax policy. While Norway is a high-cost operating market, E&P capex remains resilient with a positive outlook through 2030. Noble’s entry adds a single rig to this high-barrier market—modestly negative for Odfjell—but Odfjell’s premium semisubs remain top-tier, as reflected by $460–470k dayrates secured for Aberdeen and Nordkapp in December 2025.

I view Noble’s upgrade decision as defensible given my constructive outlook on Norwegian E&P capex, though risks remain that upgrade costs exceed $160mm and that future five-year special surveys prove costly. Separately, I believe Noble should prioritize increasing shareholder returns from 2027 onward and limit further costly rig upgrades, which it has increasingly pursued over the past three quarters.

GreatWhite’s entry into Norway does not immediately impact Odfjell’s fully contracted fleet, with 100% utilization through 1Q27 and rising realized dayrates. Odfjell’s semisubs remain highly marketable and the dividend growth story intact. However, incremental supply into the Norwegian market—including GreatWhite and potentially others—modestly lowers long-term terminal value via dividend growth assumption adjustments related to long-term dayrate upside.

Credit Relative Value: Noble’s 8.0% unsecured 2030s trade around 104 at ~200 bps spreads, reflecting strong backlog momentum but Noble’s cash flow statement will have material uses of cash in 2026 with capex for rig upgrades and likely (non-recurring) working capital draws for contract startups on various rigs. Positively, also had its four 7G drillships in Guyana extended through February 2029 by Exxon, which is great, although I do not expect credit investors to view Noble’s 2026 cash flow statement favorably. Additionally, the multiyear contracts with Shell (U.S. Gulf) and TotalEnergies (Suriname) include meaningful incentive structures that introduce risk to future EBITDA levels if not achieved. Shell is reportedly funding the Voyager and Venturer upgrades, though Noble is receiving lower fixed compensation due to incentive-heavy contract structure.

By contrast, Odfjell’s 7.25% secured 2031s trade near 102 at ~270 bps—roughly 50–70 bps wider—with exposure concentrated in Norway, a low-risk jurisdiction supported by investment-grade counterparties (Equinor, AkerBP). While I view Noble’s credit favorably, its bonds trade at tight levels for unsecured offshore drilling risk near ~200 bps of spread. For investors willing to sacrifice some liquidity, I believe Odfjell’s secured 2031s offer more attractive relative value at current levels with additional 50-70 bps.

On Wednesday, Noble and Borr closed the previously announced $360mm sale of five modern jackups, with Noble receiving $210mm in cash and $150mm in a 6-year seller’s note that PIKs the first three semiannual payments. While the transaction aligns with Noble’s strategy to focus on deepwater assets, the seller’s note is a modest credit negative. The note features a step-up coupon—7.5% (PIK) initially, rising to 10.5% after year one and up to 15% in the final year—designed to incentivize Borr to refinance the seller note. The collateral rigs are modern, marketable JU-3000N units but were uncontracted for 2026, explaining the PIK structure. The note is likely refinanced ahead of Borr’s November 2028 secured maturity, effectively making Noble a bridge creditor to a high-yield borrower rather than receive full cash proceeds, which appears to be delayed until 2027 at earliest.

Borr: Jackup drillers saw the sharpest sell-off in high-yield credit during the 2Q25 “Liberation Day” risk-asset drawdown, driven primarily unfavorable supply conditions tied to Saudi Aramco’s prior rig suspensions discussed here. Those suspensions increased warm jackup supply by more than 10% in a short period, pressuring jackup utilization and dayrates. While Aramco has begun gradually adding rigs back, the initial reduction exceeded 40 units and recent tenders have been comparatively limited in scale, leaving the market well short of 2023 tightness. That said, the deterioration has stabilized and utilization rates are improving. While I prefer deepwater floaters given stronger long-term demand growth, jackups typically offer more cyclical stability.

Borr’s secured 2028s (10.0%) and 2030s (10.375%) trade around 102.5, offering attractive mid-400s to low-500s spreads. Notably, Borr’s bonds are callable at ~102.5 on November 15, 2026. These bonds trade more than 100 bps wider than Transocean’s 2029 and 2031 unsecureds—credits I also like—highlighting compelling relative value in Borr’s secured paper. The wider spread reflect Borr’s weaker 2026 contract coverage, driven in part by jackups’ shorter-cycle contracting versus the longer lead times typical of deepwater projects. Borr faces weaker counterparty credit quality than Transocean, pressuring cash collections, but improved contracting—helped by Aramco gradually adding back rigs—should support a refinancing of these bonds.

Murphy Oil: This mid-sized E&P is Ba2/BB+ and typically trades tight, supported by a conservative financial policy and a diversified reserve base. Murphy’s boe production in 2025 was 40% Canada Onshore (Montney), 39% Offshore (mostly U.S. Gulf) and 21% US Onshore (Eagle Ford). While the lack of scale across its global reserve base draws criticism from some equity investors, that diversification is a credit positive for high yield investors. Murphy’s Tupper Montney assets are short-cycle gas reserves in a high-quality basin and would likely attract strong buyer interest if ever monetized, supporting credit quality in a downside deleveraging scenario as a source of cash.

Announcing its 4Q25 earnings Thursday, Murphy’s production guidance for 2026 of 167-175k boepd was below 182k boepd achieved in 2025. U.S. Gulf E&Ps typically factor hurricane-related downtime into guidance; 2026 reflects this assumption, while 2025 results were unaffected due to the absence of hurricane disruptions. Lower 2026 production guidance also reflects timing impacts, as the high-impact Chinook #8 well in the U.S. Gulf is expected to come online in the second half of 2026 (~15k boepd), pushing those lumpy volumes toward end of the 2026.

Murphy has had high profile exploration and appraisal outcomes recently in Vietnam and Côte d’Ivoire. In early January, Murphy reported appraisal success at the Hai Su Vang-2 well (shallow water), encountering 429 feet of net oil pay across two reservoirs and lifting recoverable resource estimates to the high end of—and potentially above—the previously stated 170–430 MMBOE range. Murphy has two more appraisal wells left in Vietnam. Murphy is targeting FID by year-end 2027, with first oil potentially in 2031. The project could be comparable in scale to Murphy’s Eagle Ford production, with upside pending further appraisal drilling.

In Côte d’Ivoire, Murphy’s first of three deepwater wells, Civette, encountered oil pay across multiple reservoirs but not at commercial quantities. The remaining Caracal (CI-102) and Bubale (CI-709) wells—to be drilled by Transocean’s Deepwater Skyros—are independent prospects with no read-through from Civette, though Civette had the highest gross resource potential. While greenfield deepwater projects can concern credit investors given the upfront capex, discoveries function as option value for Murphy, providing potential strategic flexibility by using them as a currency. Eni, which is active in Côte d’Ivoire, would be a logical potential farm-in partner for any development of Murphy’s assets in the country but Civette results likely reduce that probability.

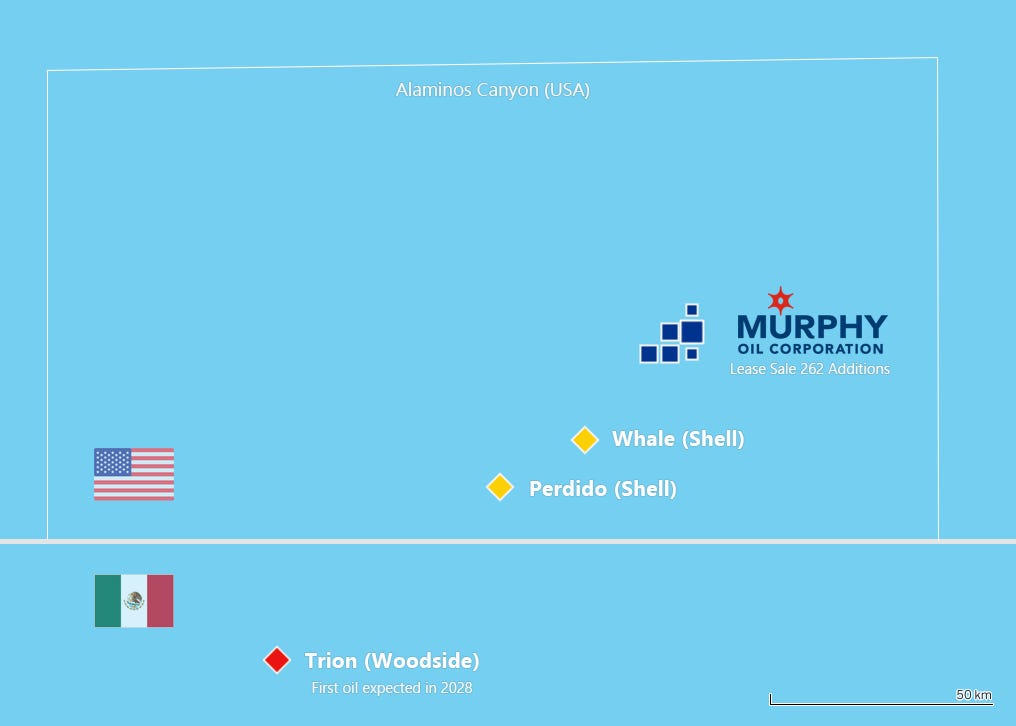

Murphy had two near-infrastructure discoveries in the U.S. Gulf in late 2025 in addition to visible project runway through 2029. Relevant to the 2030s, a key outcome of Lease Sale 262 was Murphy’s winning bids in the prospective Alaminos Canyon, a new area for the E&P. With Shell’s Perdido and Whale developments nearby and Woodside’s Trion project set to begin drilling in April 2026, Murphy’s entry into the ultra-deepwater Perdido Belt is an emerging area to watch as a potential future hub.

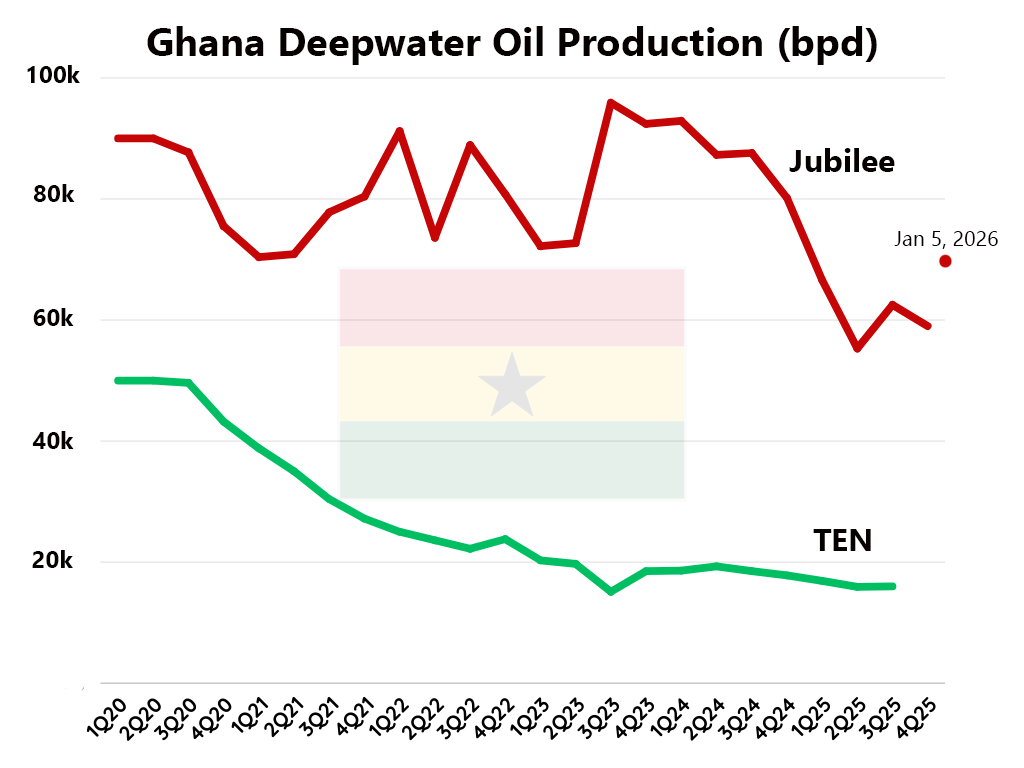

Kosmos Energy’s bonds trade at distressed levels, though the issues are small and illiquid. Its unsecured 2028s and 2031s trade at spreads above 1,500 bps, largely reflecting production challenges at the Jubilee field in Ghana in addition to weak crude oil and LNG prices.

While Tullow operates Jubilee, Kosmos holds a 38.6% interest and reported 4Q25 gross production of 59 kbpd, with output expected to start 2026 near 70 kbpd following the J-74P well coming online, though actual rates remain unconfirmed. Legacy Jubilee wells are declining at ~20% annually, implying 1Q26 production of ~65–66 kbpd absent new wells. Tullow/Kosmos have contracted the 7G drillship Noble Venturer through August 2026 to drill four additional production wells and one injector.

While expensive capital, Kosmos recently successfully raised $350mm of secured debt using its 27% interest in the Greater Tortue Ahmeyim LNG project (BP operator) to address its 2027 maturities. While I had my doubts whether they could raise debt against these assets given the geopolitical risk, GTA is now operating at capacity after coming online in 1Q25 and they recently raised a $350mm Nordic secured bond due 2031 at an 11.25% coupon, paired with a tender for $250mm of the May 2027 notes. Separately in 2H25, KOS raised $250mm in a Shell-backed secured loan against its US Gulf assets to fund ‘26 maturities. These financings extended Kosmos’ liquidity runway, allowing time for improved market conditions and better asset performance at Jubilee.

Noble’s recent $1.3B backlog update included a 50-day U.S. Gulf workover well for Beacon using the BlackRhino drillship. Given Kosmos’ disclosure in 3Q25 that the Winterfell-4 well was abandoned due to casing collapse—and that Beacon operates Winterfell with Kosmos holding a 25% non-operated interest—the award likely relates to a Winterfell workover. If confirmed, this would be a modest positive for Kosmos following the negative 3Q25 update. The workover well is schedule to commence in March 2026.

Kosmos is expected to report 4Q25 earnings in late February, providing a clearer update on the new J-74P well at Jubilee and broader production trends. While the company has made progress addressing key investor concerns around Jubilee, GTA, and near-term maturities, it remains highly exposed to oil and LNG prices. Free cash flow in 4Q25 has potential to be negative, but with Brent now near $70/bbl, both equity and debt are increasingly leveraged to recently improving commodity prices.

Tidewater: The 9.125% 2030 notes currently trade around 107–108. Debt-financed M&A risk is elevated as Tidewater has publicly expressed interest in acquiring a competitor, potentially with existing debt, though any transaction is unlikely to materially strain the balance sheet given its capacity for incremental leverage. I recommend subscribing to Misadventures in Shipping if you’re following Tidewater—the sector is opaque and specialized, and Ed covers it well.

Great find on the Winterfell block!

Had an article on Kosmos Energy published a few days before the +22% move on Friday.

Let's see what happens when Q4 2025 results are released soon.

Thanks for sharing!