Transocean-Valaris: Antitrust and HHI Analysis

Investigating global market share estimates and drillship mobility

Following Transocean's 1Q26 earnings release, regulatory approval concerns on the proposed Transocean-Valaris merger announced in February have come into sharper focus. Before turning to market share analysis, it is worth noting that current dayrates, the clearest market signal competition via supply and demand, remain well below levels required to earn drillers' true cost of capital.

The current market for 7G drillships indicates dayrates in the low $400k’s, relative to the ~$600k level estimated for offshore drillers to earn their true cost of capital when originally ordered in 2010-2014. Dayrates remaining well below $600,000 is itself evidence of a competitive market. All else equal, the proposed Transocean-Valaris merger would be supportive of higher dayrates, although the combined entity would still compete against Noble, Seadrill, Stena, Saipem, regional drillers including Odfjell, Constellation, Foresea and Ventura, as well as smaller 1-3 rig owners who generally bid more aggressively for utilization.

On Tuesday’s earnings call, Transocean provided additional detail regarding the proposed merger:

The merger requires antitrust clearance in seven jurisdictions.

Saudi Arabia and Trinidad & Tobago have already approved, leaving the U.S., Angola, Australia, Brazil and Egypt outstanding.

Transocean disclosed receipt of a U.S. Department of Justice second request for additional information, which management characterized as the DOJ needing more time to understand post-close competitive dynamics.

The company reiterated its expectation for a second half 2026 close.

Transocean generally characterized the DOJ review process as constructive, noting they are helping regulators understand their U.S. Gulf operations and the broader global market. They described the conversations as going "very well,” although the stock market’s weak reaction to a decent quarter indicated skepticism toward the deal closing on schedule as anticipated.

Qualitatively, I believe the Transocean and Valaris fleets complement each other well with little overlap in terms of specifications. Transocean has two 8G drillships and Valaris has none. Transocean and Valaris both have large 7G drillship fleets, but the majority of Transocean’s 7G’s are 1,400 st hookload and Valaris’ are 1,250 st hookload. Transocean has seven harsh environment semisubs eligible to work in Norway and Valaris has none. Valaris has a large shallow-water jackup fleet, whereas Transocean has none. A key distinction between the two companies is Transocean's Norway-eligible semisub fleet, which has underpinned recent earnings strength given relative market resilience there. Valaris, by contrast, carries greater West Africa exposure with its 7G drillship fleet, a comparatively softer market through 2025 and into 1H 2026, contributing to more recent white space and earnings weakness.

I believe the proposed Transocean-Valaris merger creates a globally diversified fleet by specification and region marketability, although regulators may have a different view. The Valaris and Noble fleets have considerably more overlap due to heavy standard 7G drillship concentrations than the Transocean and Valaris fleets.

Herfindahl-Hirschman Index Review

I am not an antitrust attorney. I am simply applying analysis from the Herfindahl-Hirschman Index (HHI) as a barometer for industry competition post-merger. The HHI is a standard tool used by antitrust regulators to measure market concentration. It is calculated by summing the squared market shares of every competitor in a defined market, producing a score between 0 and 10,000, where higher scores indicate greater concentration.

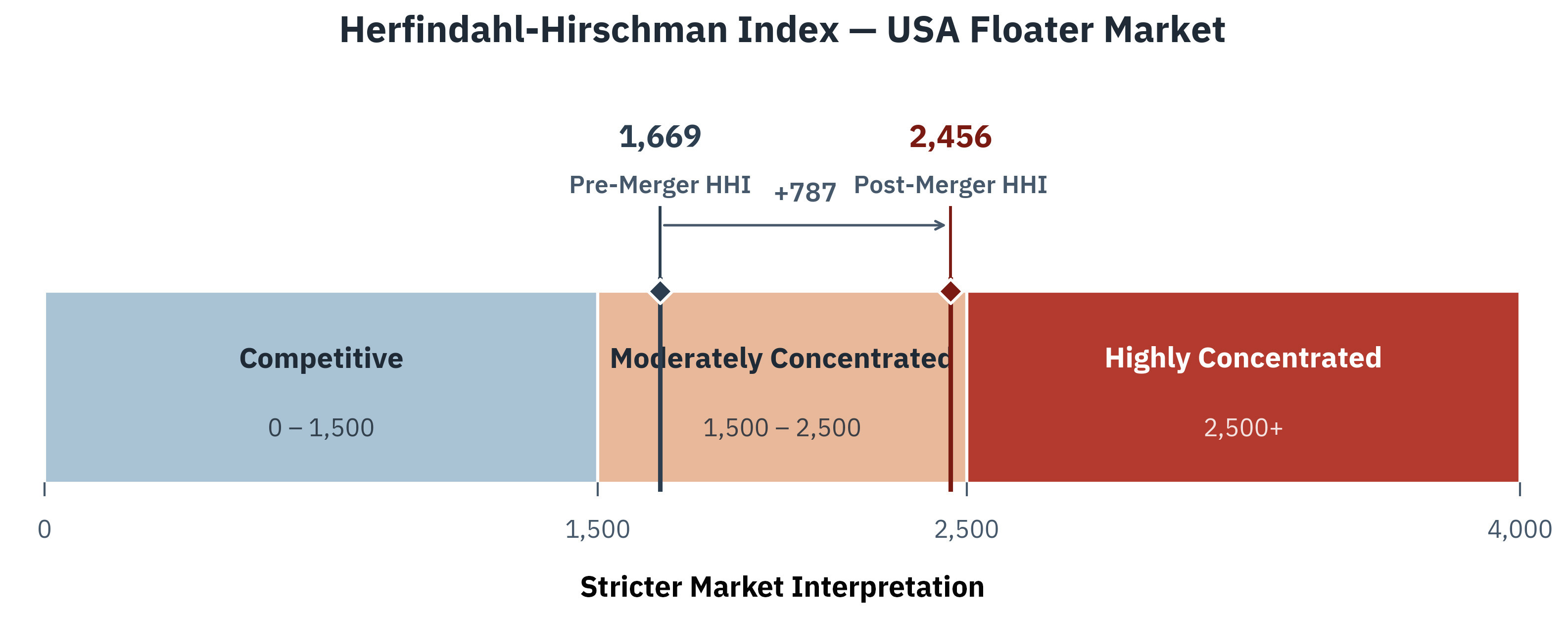

U.S. regulators apply three thresholds: below 1,500 is considered competitive, 1,500–2,500 moderately concentrated and above 2,500 highly concentrated. Regulators evaluate not just the absolute post-merger HHI but also the increase in HHI caused by the merger with increases above 200 points yielding more regulatory attention. Considering the estimated HHI is increasing by 600-790 from the proposed Transocean-Valaris merger, it is not surprising the US DOJ is requesting additional information. Given the DOJ's second request, the following analysis focuses on the U.S. market.

Unlike tankers, drillships and semisubs carry hundreds of millions of dollars of specialized equipment that creates meaningful differences in regional and job-specific marketability by rig, which complicates market share analysis and is a material limitation of the HHI analysis. For example, in the U.S. Gulf, there are a few 8G drillships capable of 20k psi completions (very high specification), many 7G/7G+ drillships and a couple rigs that mostly do intervention, workover and P&A work.

More broadly, semisubs are engineered for harsh environments, predominantly Norway, where drillships do not operate. Drillships dominate the “Golden Triangle” of the U.S. Gulf, Brazil and West Africa, while also serving more benign-environment deepwater markets including Guyana, Indonesia and Mozambique — this is a global market.

The market for deepwater rigs (aka “floaters”) in the U.S. Gulf is dominated by the highest specification drillships in the world, many of which Transocean owns. Of the 20 deepwater rigs currently located in the U.S. Gulf, Transocean and Valaris collectively own nine — a combined 45% market share. Noble holds six rigs (30%), Seadrill three (15%), and Stena one (5%). This yields a U.S. Gulf HHI of 3,175, categorized as "highly concentrated," but a regional calculation is the wrong framework. Drillships are globally mobile assets marketed across multiple regions simultaneously. Transocean's most recent fixture, the Deepwater Asgard moving from the U.S. Gulf to the East Med, is a prime example of why the relevant antitrust market should be defined globally rather than regionally.

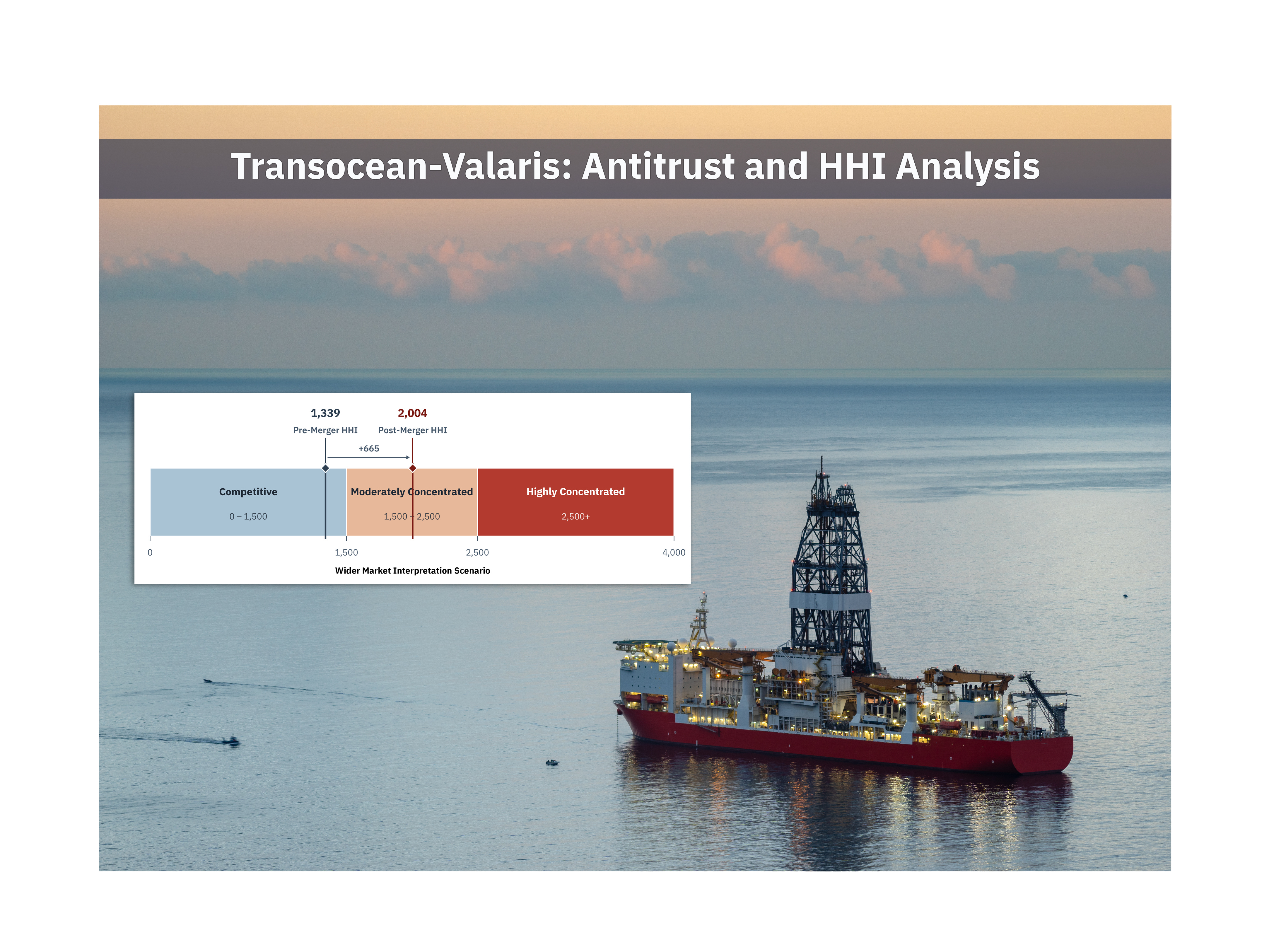

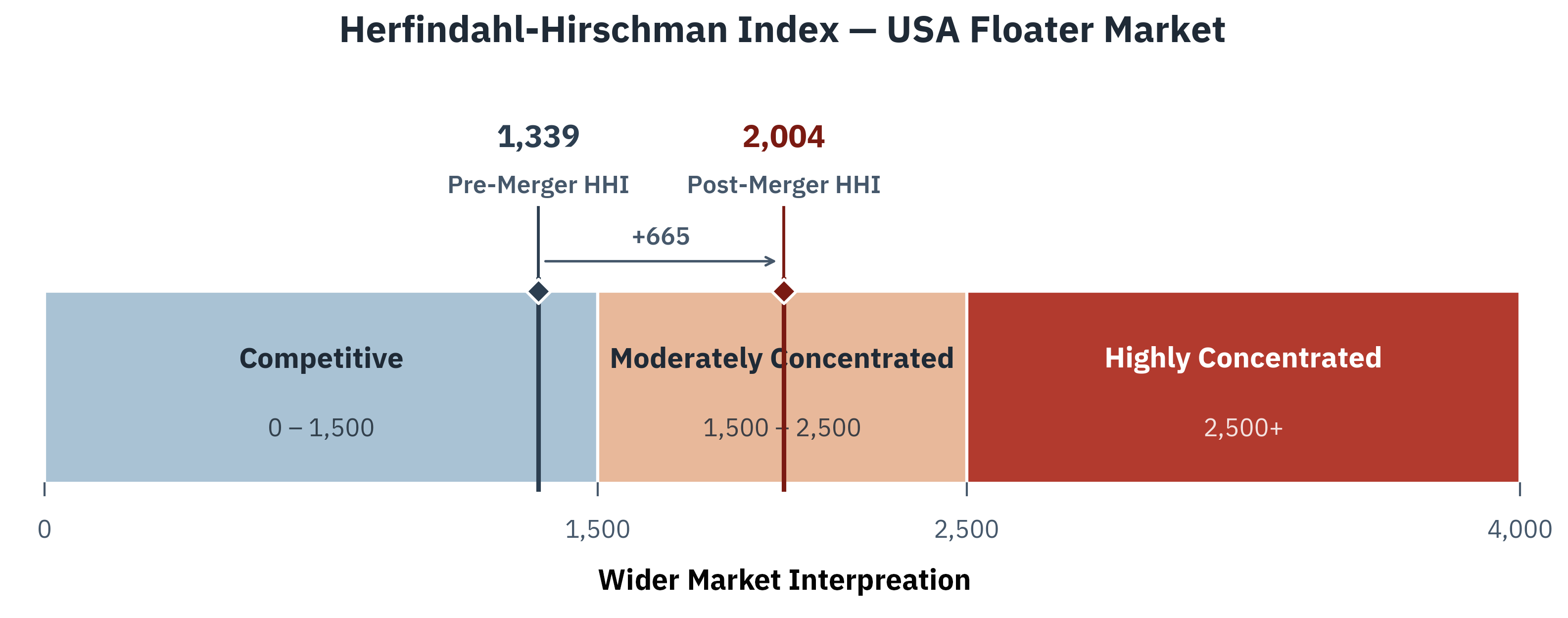

Given the inherent subjectivity of market definitions in a specialized deepwater rig market, I present two HHI scenarios: (1) A Stricter market interpretation and (2) a Wider market interpretation.

(1) Stricter Market Interpretation: Includes 7G and 8G drillships, as well as higher specification 6G drillships with two blowout preventers (BOP) and managed pressure drilling (MPD) which are arguably competitive in the US Gulf. I have included some higher specification semisubs that could reasonably work in the US Gulf, although excluded those currently operating in Norway.

The HHI of 2,456 indicates it is close to the “highly concentrated” designation, although still fits within an arguably acceptable “moderately concentrated” definition. Regulators become concerned when large entities potentially corner the market on limited supply, although the reality is the floater market is global and rigs can be moved to more attractive markets if economics support. Drillships are particularly mobile because they are more self-propelled than semisubs.

(2) Wider Market Interpretation: A separate group of deepwater rigs owned by regional drillers could theoretically work in the U.S. Gulf if demanded, which includes Odfjell (Norway), Constellation (Brazil), Foresea (Brazil) and Ventura (Brazil). The Odfjell semisubs are designed for the Norwegian Continental Shelf and very unlikely to leave, but if economics supported it they theoretically could work in the US Gulf. Additionally, Brazilian regionals own fleets of 6G drillships which are lower specification “workhorse” rigs in Brazil, but would be capable of working in the US Gulf with some upgrades if needed. The Brazilian regionals tend to only work in Brazil, but there have been instances where their rigs were bid internationally.

The HHI analysis above incorporates regional drillers and wider set of lower spec 6G drillships — an important inclusion and yields a “moderately concentrated” measure of 2,004. If the DOJ is concerned about Transocean-Valaris cornering the global floater market, regional players represent a meaningful source of competitive backstop supply that would constrain any anticompetitive pricing behavior post-merger.

Summary

While the proposed Transocean-Valaris merger increases industry concentration meaningfully, the market share analysis indicates the global market arguably fits into a “moderately concentrated” category. Given the material shift in market concentration the proposed combination would produce, the DOJ's second request for additional information is not a surprise.

This analysis is intended as a framework, not a regulatory assessment — actual outcomes will depend on how the DOJ defines the relevant market, who are likely to define the market differently. I fall back on a simpler high-level analysis I mentioned at the beginning of the article, whereby I believe Transocean (8G drillships, 7G+ drillships, Norway-eligible semisubs) and Valaris (standard 7G drillships and jackups) have complementary fleets with little overlap. The two are more of a natural fit to create a globally diversified offshore drilling company than creating an excessive concentration in any particular rig specification that would be anticompetitive.

When it comes to regulation, there is risk of the deal not reaching regulatory approval although Transocean’s commentary on their 1Q26 call was constructive, but noted outstanding requests. Sometimes regulatory approvals may require asset divestitures, which would add a layer of complication and potentially delay the deal from closing by 2H26.

In terms of timing, Noble Corporation announced the acquisition of Diamond Offshore on June 10, 2024 with the expectation of the deal closing by 1Q25. The deal closed meaningfully ahead of schedule on September 4, 2024. While Diamond was a smaller offshore driller than Valaris, this is evidence of a global acquisition getting done on time. Whether Transocean-Valaris follows a similarly expedited path will ultimately depend on how the DOJ resolves its market definition questions, as well as other countries yet to give regulatory approval.

Supplemental Market Analysis

In addition to the USA, Brazil was noted as one of the countries for which regulatory approval was still outstanding. Brazil is the world’s largest deepwater rig market with its success in the Santos and Campos Basins. While I can’t speak for the regulatory process in Brazil which can scrutinize mergers, Brazil is a competitive deepwater rig market which includes three regional drillers (Constellation, Foresea and Ventura) which primarily operate in Brazil. The proposed Transocean-Valaris merger should not change the competitive landscape in Brazil that materially. Angola, Egypt and Australia are also still outstanding regarding their regulatory reviews.

Thank you to @ICBarrett on Twitter/X for quickly notifying me of his market interpretations regarding regulatory concerns.

Nice presentation, thinking that not many lawyers at the DOJ have even a beginners concept of complicated, how specialized the deepwater sector is, how essential to national security this sector will become as the world energy markets become more regionalized, moving away from the Arabian peninsula. Tommy you may need to become a lobbyist for the entire sector.

Great article - thanks Tommy!