Offshore High Yield: Tidewater, Transocean, Azule and Others

Tidewater M&A in Brazil, Transocean Capital Structure, Jubilee Update and Miscellaneous High Yield Relative Value

In This Issue:

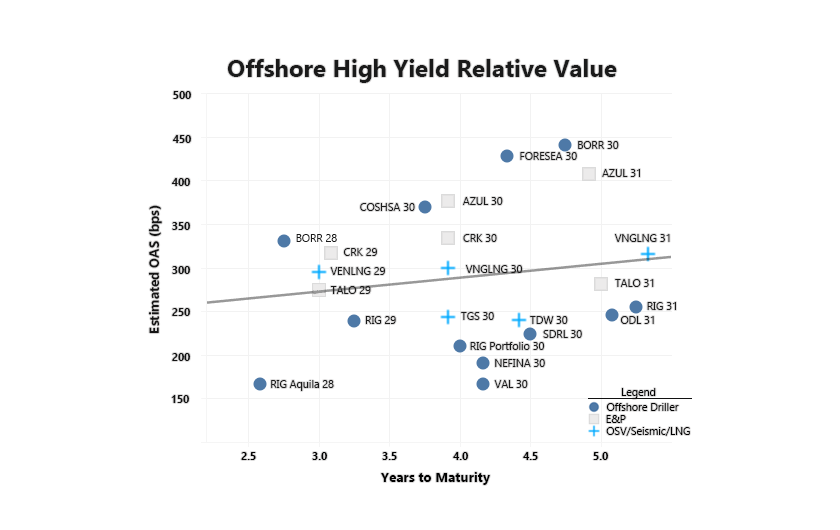

High Yield Relative Value: Transocean, Azule Energy, Comstock Resources (shale), Foresea, and Borr

Tidewater’s acquisition of Wilson Sons Ultratug Offshore

RIG/VAL Post-Merger Capital Structure Thoughts

Jubilee (Ghana) deepwater field update for Kosmos

Deepwater driller credits are performing well. The pain of 2H24-2025 was primarily driven by project delays and resulting rig idle time. In Midyear 2025 Outlook, cautious optimism on the drillship market existed regarding projects moving forward although it was too soon to celebrate because project slippage was still possible. Since then, the picture has improved materially, with DS-12 (Egypt), Gerry de Souza (Nigeria), Capella (Malaysia), Skyros (Australia) and others all securing contracts, and good visibility on additional multiyear awards moving forward without material delay.

Underpinning this constructive backdrop, Oil majors — particularly European players without significant US shale exposure — have remained constructive on E&P capex, with long-cycle deepwater projects largely insulated from budget cuts. While lower oil prices have prompted some capex reductions, the pullback has been concentrated in alternative energy rather than E&P, as reserve replacement has become an increasing focus after years of gradual decline.

Transocean’s unsecured 2029s and 2031s (Caa1/B-) rallied by ~110 bps after the all-stock Valaris acquisition was announced on February 9th. Noble/NEFINA and VAL 2030s both trade inside of 200 bps and I believe better relative value opportunities exist. Within offshore drilling, Odfjell’s new secured 2031s offer 50-60 bps more of spread and have high-quality collateral rigs.

Azule Energy (B2) is a 50/50 BP/Eni JV formed in 2022 and a first-time high yield issuer as of January 2025. The ~$3.5B EBITDA E&P produces primarily from Angola's Block 15/06, neighboring ExxonMobil and TotalEnergies' production hubs, and operates PEL 85 in Namibia where its Capricornus discovery is arguably the basin's best to date. Further, Rhino reported 'excellent reservoir deliverability' at the Volans-1 well on PEL 85, advancing the discovery toward potential development although gas levels are an early concern and discoveries still require appraisal. Azule commands a spread premium given its concentrated portfolio and new issuer status, though early execution has been strong — most notably delivering the Agogo FPSO six months ahead of schedule. More to follow on Azule in the future.

Comstock Resources (B3/B) is a Haynesville pure-play E&P whose unsecured bonds widened 80-100 bps since its 2026 capex guide came in at ~$1.5-1.6B, well above the ~$1.1-1.3B consensus as it aggressively develops its higher-upside Western Haynesville acreage. Leveraged but well-positioned near Gulf Coast LNG export infrastructure, the spread widening may represent an attractive entry point for investors constructive on natural gas and LNG export demand.

Foresea (B2/B+) announced a distribution to shareholders in early February to be funded by a tap of its 2030 secured notes, which saw the bonds’ credit spreads widen from ~380 bps to ~425 bps as of February 22, 2026. Foresea is a regional driller in Brazil with five 6G rigs contracted to Petrobras. Foresea holds a strong incumbent position in Brazil, though the company is rumored to have recently been marketing a 6G drillship internationally.

While shallow-water driller Borr (B3/B) has seen its bonds rally from oversold levels in 2025, the bonds still carry meaningful spread premium over the large deepwater drillers. In December 2025, Borr acquired five jackup rigs from Noble for $360mm — three of which were uncontracted for 2026. To offset carry costs on the idle rigs, Borr structured part of the purchase with a seller's note that PIKs interest for the first 18 months — 7.5% for the first 12, stepping up to 10.5% thereafter.

Tidewater Acquires Wilson Sons Ultratug Offshore

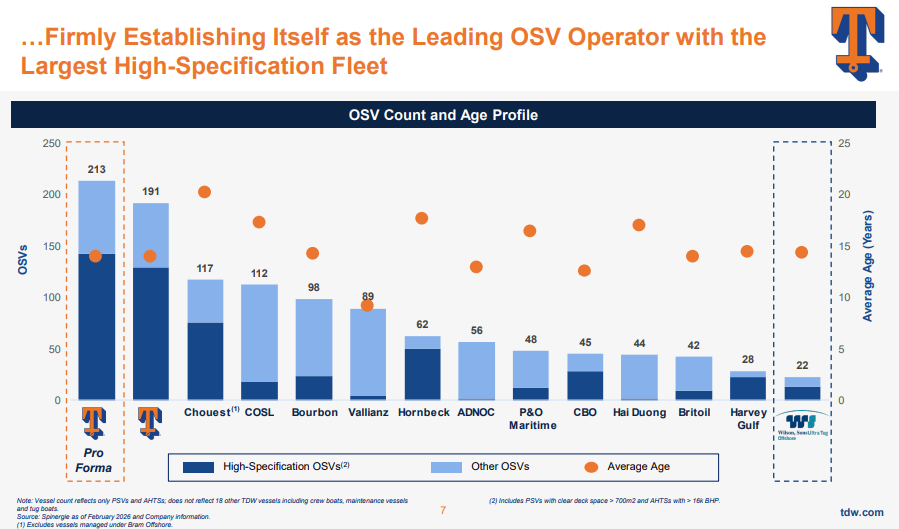

On Sunday, Tidewater announced the $500mm acquisition of Wilson Sons Ultratug Offshore, a Brazilian OSV operator, which includes assuming $261mm of debt and the remaining funded with cash. The equity market’s initial reaction was positive given its all-cash nature and post-close leverage is expected to remain below 1.0x net debt/EBITDA.

While the deal carries no expected cost synergies, Tidewater gains more than 22 Brazilian-built OSVs and also gains option value to market its international fleet within Brazil, where local laws favor domestic service providers which it now qualifies for with Wilson Sons.

Brazil is the world’s largest deepwater services market, with near-term growth supported by the Búzios field ramp-up in 2027 although the growth trajectory beyond that remains less certain given the absence of other obvious mega-field FIDs. The most consequential exploration activity is on Brazil’s Equatorial Margin, though the high-profile Morpho well has faced delays since spudding in September 2025, underscoring the region’s execution risk.

Tidewater has long targeted Americas fleet expansion and younger average fleet age. While Wilson Sons does not reduce the fleet age, it achieves improved Brazilian market access via the acquired fleet and marketing option value for its existing fleet. A US Gulf acquisition (i.e. Hornbeck or Harvey Gulf) was effectively ruled out on the Q&A call. Grupo CBO would have been a larger bite into the Brazilian OSV market, but its large size and higher debt levels (~3.3x net leverage) would have consumed more balance sheet with the debt potentially eating into future budget for buybacks, opportunistic M&A and future capex investments. Wilson Sons achieves improved access into Brazil at a lower balance sheet cost — arguably the more attractive outcome for both credit and equity.

As noted above, acquiring younger high-spec OSVs is a challenge. With average industry fleet age around 14-15 years, a newbuild cycle is definitely not urgent today but the industry needs to begin planning for one toward decade-end as assets approach 20 years. Vessels will operate beyond that threshold, but escalating maintenance costs make a prolonged deferral risky if it results in a compressed newbuild cycle in the 2030’s. Below 1.0x net leverage today, Tidewater is well-positioned but M&A options to meaningfully reduce fleet age are limited.

RIG/VAL: What Does the Post-Merger Capital Structure Look Like?

Transocean's all-stock merger with Valaris is expected to be materially deleveraging, with close anticipated in 2H 2026 pending shareholder and regulatory approvals. A post-close refinancing of RIG's capital structure appears likely. The existing secured debt stack is a significant impediment to shareholder returns, with secured bond indentures requiring at least $322.5mm in principal amortization during 2026 (more including a shipyard loan on Atlas) and hundreds of millions locked up in restricted cash.

February 2027 could be an ideal time to refinance its secured bonds as call premiums reduce, but the big question is what will Transocean’s new debt stack look like? Will the high yield market support an all-unsecured capital structure?

As an asset-heavy company with potentially unencumbered high-spec rigs, Transocean could use the secured market to reduce its cost of capital although the ultimate attractiveness will depend heavily on the terms credit investors demand.

While I previously viewed the borrower-friendly ~$1.5T leveraged loan market as effectively closed to Transocean, the Valaris merger and technological disruption to software credits could open this as a viable financing option post-close. CLOs absorb roughly two-thirds of leveraged loan supply, but their historically poor experience with offshore drillers, structural aversion to cyclical oilfield services companies and especially Transocean's current Caa1 rating make them unlikely buyers today — CLOs face penalties once Caa-rated loans exceed 7.5% of collateral.

A post-merger upgrade from Moody’s Caa1-rating appears likely and the timing may be favorable. Software & Services represents ~11.4% of CLO collateral (Eagle Point, September 2025), and as the weakest borrowers face CCC-downgrade risk from technological disruption, CLO managers will reduce those exposures. With LBO-driven supply constrained since the Fed began hiking rates, CLOs are actively hunting for quality exposure elsewhere. While I recognize the challenges, I believe a combined RIG/VAL is stronger credit quality than many others in the LevLoan space. A B2/B rated post-merger entity could be a compelling fit given Transocean avoided bankruptcy (important for CLO’s) and is fundamentally in a stronger industry position than a decade ago.

The typical Term Loan B offers borrower-friendly terms: 7-year maturity, 1% amortization, minimal financial covenants, and only 6-month call protection versus the 2-year non-call standard in high yield. Transocean would likely face amortization above the 1% TLB floor, though well below the 7% in Odfjell's most recent secured bond, but would be an attractive source of secured financing given its looser terms.

Kosmos - Jubilee Field Update

I first covered the Jubilee Field in Ghana as an example of deepwater reservoir technology management with publicly observable results to follow. Operator Tullow faced significant production challenges from investment deferrals and related reservoir management missteps, but has since embraced 4D seismic and OBN technology alongside a targeted infill drilling program using the Noble Venturer (7G drillship). Early results are encouraging.

The first infill well (J72) came online in July 2025 producing ~10k bopd, followed by J74 which exceeded expectations, ramping to ~13k bopd. This has lifted gross Jubilee production to over 70k bopd month-to-date in February. The J75 well encountered ~40m of net pay across three zones — consistent with J72 and J74 — and is expected to begin producing by end of March

Another 4-5 wells remain in 2026 with Venturer contracted through August. Legacy well decline rates of ~20% annually will continue to weigh on overall production, but the field is demonstrating meaningful remaining productivity with two successful producers, a promising third and more wells still ahead.

Tommy, thanks. Do you know of any ETFs that include some of the high yield bonds mentioned above?

Thanks for this -

I thought TDW guided for Wilson Sons at $220m revenue, 58% GM and $14m SG&A - so $113m EBITDA… maybe I missed something?