"Exploration is Back"

E&P Capital Discipline Remains but Incrementally Positive Signs for Rigs

On April 20, 2026, Goldman Sachs published a note to clients on E&P’s prominently stating, “The market is rewarding reinvestment again” and “the industry needs to reinvest in reserve life”. On Thursday morning, leading marine seismic data company TGS boldly declared that 'Exploration is Back.' While there is an element of self-promotion in that claim, TGS CEO Kristian Johansen has also recently given brutally honest commentary when markets have been weaker.

Is exploration really back? There are important caveats. Exploration decisions made today won't translate into drilling activity in 2026. These are 2027 stories at the earliest with some campaigns extending into 2028. This does not happen overnight and E&P’s will remain disciplined with investments. For deepwater oil rigs, exploration tends to be shorter-term contracts. Development drilling tends to be multiyear work and more impactful to rig market, but a few extra exploration jobs in 2027 can absorb some supply and provide foundational support for dayrate appreciation.

You can never be too sure of anything in oil and gas.

Base Case (75%) : Modest increases in exploration budgets worked in to 2027 capital budgets as IOC’s seek to leverage technology instead of pure $ spend.

Bull Case (15%) : Wildcatting is back. Oil majors commit themselves to exploration campaigns through the end of the decade.

Bear Case (10%): I would not even want to buy TGS high yield bonds.

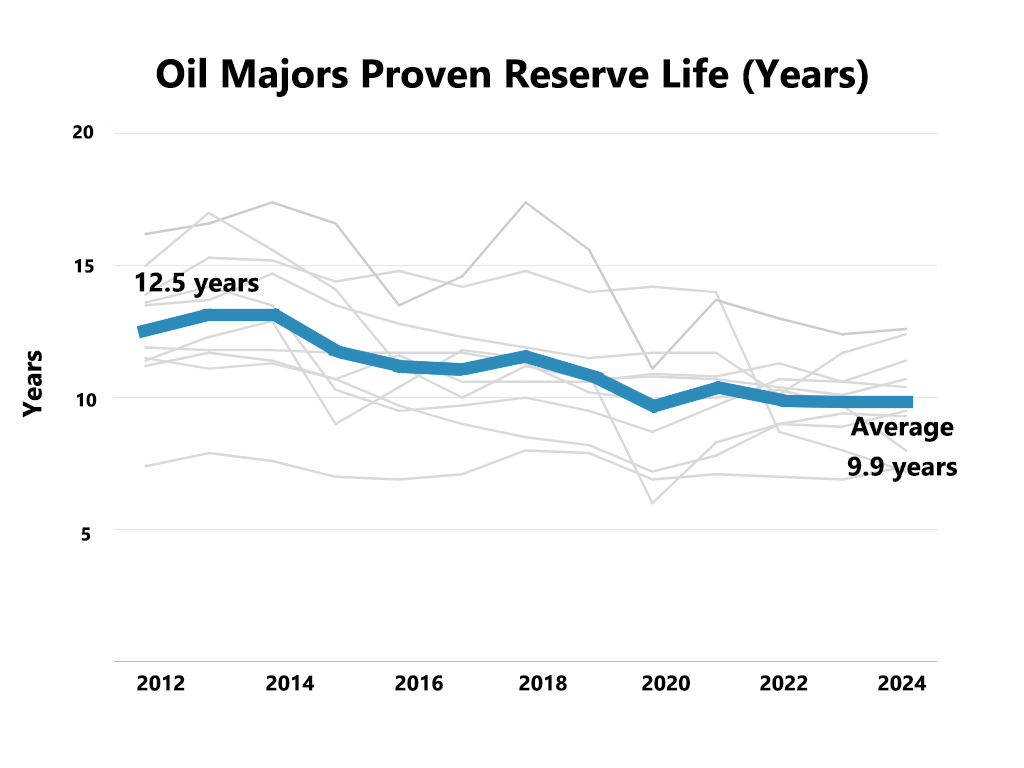

Oil majors are valued on their dividends and dividend growth, a commitment they generally describe as sacrosanct. The 'capital discipline' doctrine that followed OPEC's market-disrupting 2014 price war drove a decade of brownfield-heavy investment, leveraging existing infrastructure with more limited frontier exploration. After a decade of restraint, IOC’s have delivered strong dividends and buybacks, but reserve life has quietly eroded from roughly 13 years to ~10 years.

Oil majors should not resemble royalty trusts. They create value by investing capital into developing oil reserves that produce positive cash flows at scale that generate IRR’s above their cost of capital, which is the foundation of their dividend growth that matters so much to their valuation.

It’s still too early for oil majors to increase their capital expenditures which were set late in 2025 in their capital budgets for 2026, but discussions for the 2027 capital budget are likely beginning. The oil market can change dramatically off a social media post, so IOC’s will likely remain cautious and plan for different scenarios. The shape of the futures curve is heavy backwardation with spot prices well above futures prices with Brent spot at $108/bbl (as of May 1, 2026) and Brent futures prices between $71-$75/bbl from 2028-2030. One dynamic that is becoming increasingly clear is that global oil inventories are steadily drawing down by the day, a trend that should provide a supportive price backdrop going forward.

Deepwater Exploration - It never went away

One of the exciting things about Deepwater are the technology advancements that have made producing oil and gas at >1,000m water depths economical and there are still various frontier regions across the globe with prospectivity. Petrobras is currently drilling the Morpho exploration well on Brazil's northern Equatorial Margin (pictured below), in the Amapá region, using Foresea's ODN II drillship. The basin has drawn significant interest from oil majors — Chevron and ExxonMobil acquired blocks in the Foz do Amazonas ('mouth of the Amazon') in June 2025 — where Amazon sediment deposition over hundreds of millions of years created potentially prolific hydrocarbon systems. Morpho has experienced drilling delays, with results now expected in Q2 2026. Morpho is the definition of a high-impact, play-opening exploration well, but even if unsuccessful there will be additional wells to follow in the region.

Just because the spot price of oil is >$100/bbl doesn’t mean oil majors are rushing to go explore for oil in frontier regions of the world in 2H26. Chevron and Exxon just acquired the Foz do Amazonas blocks and will likely wait to learn from Petrobras' exploration results before committing to an exploration campaign in the region. Separately, the wheels are already in motion for upcoming exploration wells for both, as Chevron is expected to drill two wells in Namibia’s PEL 90 and 82, among other regions such as the East Med and potentially Uruguay. Exxon tends to not disclose much information, but one high impact well for them will be the Asopus gas prospect in Greece’s Ionian Sea.

Deepwater capex is inherently long-cycle. Oil majors commit billions to greenfield projects years before generating positive free cash flow, creating meaningful time-value drag on IRRs and NPVs. That said, time-to-first-oil has compressed materially since the 2010–2014 cycle, driven by elimination of engineering redundancies, design standardization and simplified project scopes. The 2016 Technip/FMC Technologies merger was a structural catalyst for this improvement, and TechnipFMC (NYSE: FTI) remains focused on compressing cycle times further. A consistent theme from oil company management teams is AI's impact on seismic data processing — accelerating interpretation timelines and compressing exploration cycle times by months.

Equity markets have rewarded capital discipline from oil majors and E&P, and while oil majors will continue to be smart with capital investments, questions from equity analysts on oil major conference calls regarding concerns on reserve life are becoming more common. Transocean’s current CEO, Keelan Adamson, commented at the SB1M conference in 1H 2025 that the oil major capital discipline has been keeping dayrates from reaching their full potential, but if/when oil majors begin to shift their focus on reserve replacement is when there can be persistent dayrate improvements.

The reduction in proven reserve life has been well-documented by various sources. Oil majors will seek to replace reserves with different sources of hydrocarbons, as evidenced by Shell’s recent acquisition of ARC Resources in Canada. UAE’s exit from OPEC+ this week also could open up unconventional opportunities for reserve replacement. It’s still early with Venezuela but the country’s large undeveloped reserves could also serve as a source of reserve replacement. Deepwater will remain a meaningful source of reserve replacement, particularly for European IOC’s, as technology advancements have improved its cost structure over the last decade.

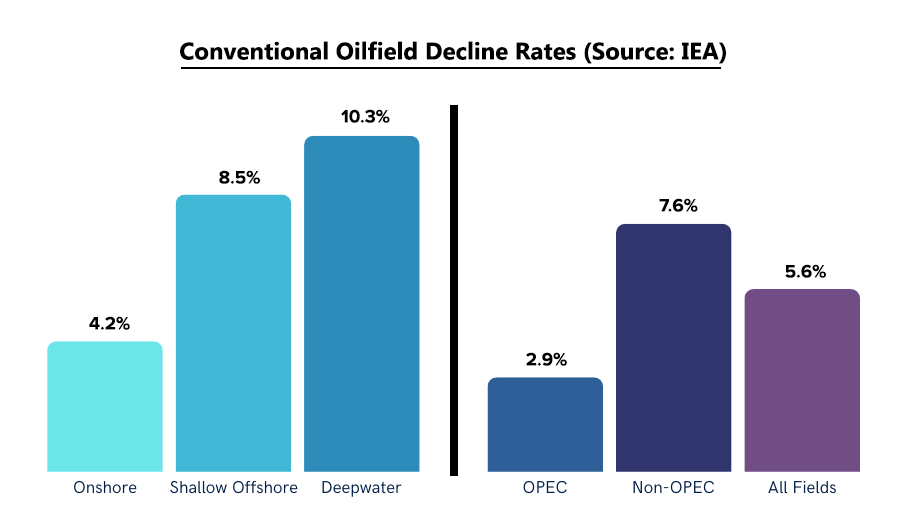

Deepwater field decline rates vary widely, from low-to-mid single digits to 20% annually, making generalization difficult. That said, elevated decline rates are generally constructive for rig demand: as production falls, operators have incentive to drill low-cost subsea tieback wells to fill spare FPSO capacity, leveraging existing infrastructure to offset decline at a lower cost than greenfield capex.

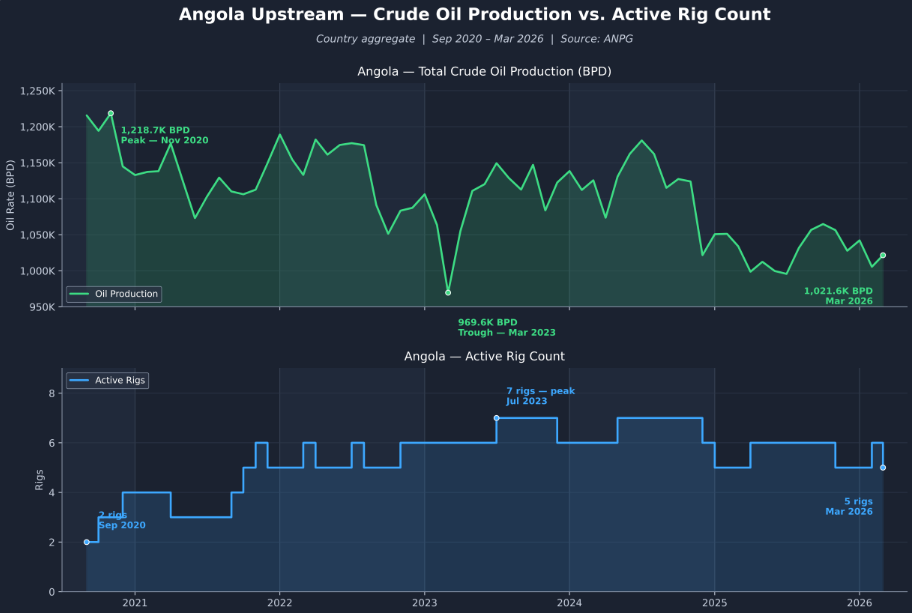

The consequences of a decade of underinvestment are perhaps nowhere more visible than Angola, which has experienced underinvestment and production is currently ~600k bpd below its peak levels in 2013-2014. Angola’s oil production is almost entirely sourced via deepwater. This week a key operator in Angola, TotalEnergies, made a positive comment regarding potential investment appetite to add a rig in Angola in response to higher oil prices.

Deepwater Rig Market Updates

TotalEnergies’ 1Q26 earnings release noted, “the Company is evaluating options to accelerate short cycle investments to capture the current hydrocarbon price environment.” On the conference call, Total mentioned Angola as a source of short-cycle options although this depends on rig availability (positive commentary for rates). TotalEnergies is operator of various FPSO’s in Blocks 17, 17/06 and 32 in Angola that produce 400k bpd (Total may have only ~30-40% operator interests of this amount), which would be shorter-cycle, low-cost brownfield infill drilling options. These would not be large investments but would offset decline at existing wells, and hiring an additional drillship for associated infill drilling should be well-received by investors in a higher oil price environment. Separately, TotalEnergies also made an attractive farm-in agreement with Galp Energia in December 2025 for a 40% interest in PEL 83, an attractive greenfield option for which they will begin a multi-well appraisal program late in 2026.

Shell should consider contracting a 7G drillship for infill drilling across its Mars, Olympus and Ursa platforms in the US Gulf. While the US is predominantly associated with light sweet oil, the Mars-Olympus-Ursa complex produces medium sour crude — a grade currently commanding approximately $118/bbl, a meaningful premium to Brent at $109/bbl. Perhaps beginning a drilling program when hurricane season ends is something shareholders would like considering elevated oil prices from a crude grade in high demand. Separately, Shell is also expected to commence an exploration campaign next year in Angola where the geology draws comparisons to Brazil's pre-salt discoveries, although significant exploration and appraisal work remains before the resource potential can be properly assessed.

Longer-cycle development programs appear to be proceeding on schedule, but it is the shorter-term, opportunistic infill campaigns — enabled by in-place infrastructure — that could flex up floater demand more quickly than greenfield programs in other regions. A handful of incremental infill programs materializing in 4Q26 and into 2027, combined with exploration campaigns planned for 2027–2028, could play a meaningful role in tightening floater utilization and providing dayrate support as the longer-cycle development pipeline builds.

Thanks for the update and overview on the state of deepwater market Tommy. Any thoughts on the RIG/VAL merger as supportive of higher day rates or is it still too early to say? Also, although it isn’t a deepwater topic, any comments on the massive Vaca Muerte shale play in Argentina? I’m watching CVX, YPF, VIST, and HAL for insights on that one.

Exploration sounds like it’s back.

The reality is how long it takes to actually show up.