Deepwater in 2026

7G+ Drillships, Cost Structure, Consolidation, Norway, "Scrap, Baby, Scrap" and Deepwater FID's

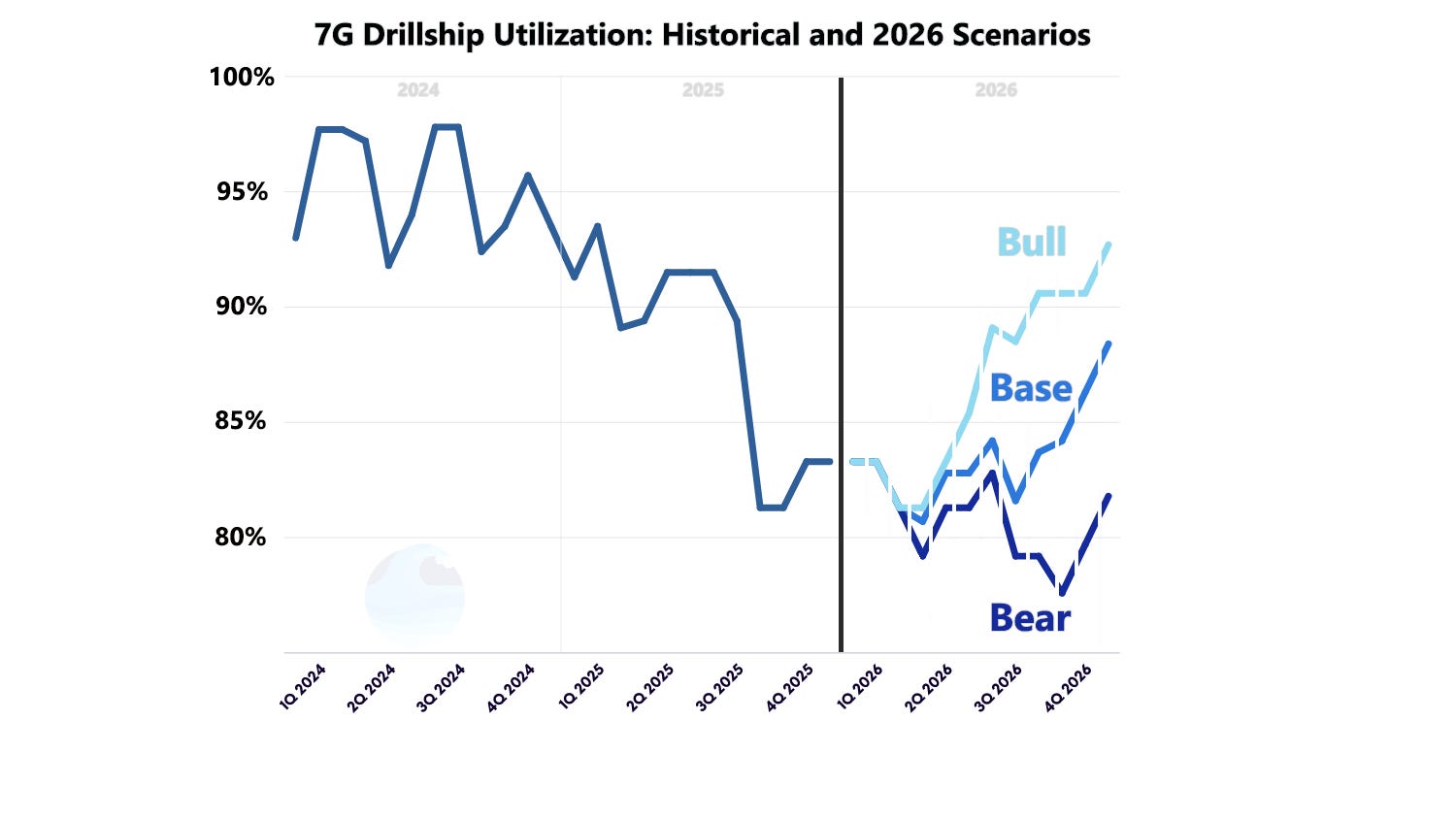

Executive Summary: Deepwater fundamentals are stabilizing following a mid-cycle correction, with 7G utilization likely bottoming in the low-to-mid-80% range. While near-term dayrate upside remains constrained by utilization-driven bidding and soft oil prices, visibility into 2H26–2027 is progressing mostly as anticipated. Key 2026 watch items include RIG’s 7G+ contracting, consolidation potential, Norwegian market and potential deepwater FIDs in Namibia, Indonesia and Mozambique.

Despite persistent concerns about oil price weakness, the deepwater drilling market has defied pessimistic forecasts throughout 2025. The long-cycle nature of deepwater contracting provides nearly a year of visibility, aligning with equity markets’ 12-month forward focus. Drilling equities weakened from September 2024 amid rising idle time, pressuring earnings as outlined in the Drillship 2026 Outlook. Despite weak oil markets, equities recovered from 4Q24–2Q25 lows as 7G drillship utilization stabilized, supported by a rebound in West Africa. While near-term Petrobras tender awards are unlikely to show dayrate improvements as some drillers prioritize utilization, markets are forward-looking, with utilization expected to recover in 2H26 and into 2027—suggesting low-to-mid-80% utilization represents the mid-cycle trough and should support future dayrates.

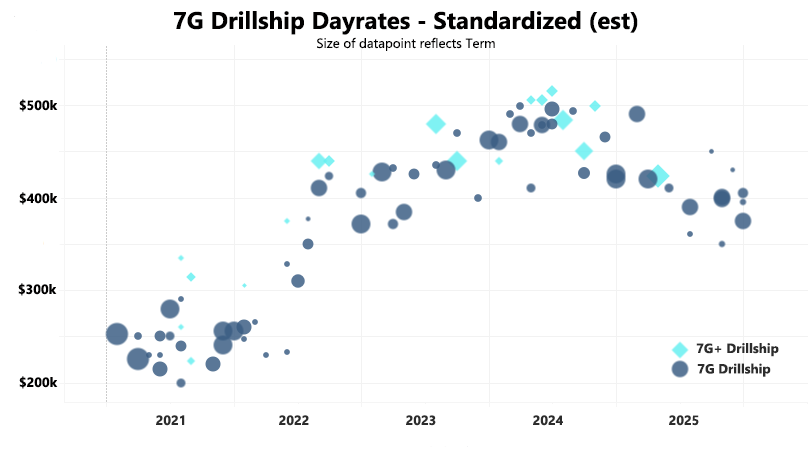

Pareto Securities, a well-regarded Nordic investment bank, released a client survey in early May 2025 polling “Dayrate expectations on upcoming 7G/leading-edge contracts,” with responses as follows; $200k (7%), $250k (53%), $350k (40%) and $400k (0%).

The negative sentiment was apparently driven by extrapolating the prior cycle (2015-2016) downturn when dayrates fell from the $600k range to the $200k’s. The major difference in the current cycle vs the last cycle is the market had to absorb a newbuild cycle that overestimated drillship demand when orders were made – oil was $100/bbl in 2011-2013. When OPEC increased production in late 2014, oil prices fell to the $40’s and newbuild deliveries overwhelmed the market for years. Further, E&Ps began to favor short-cycle, flexible capex as the Permian Basin was about to add >3 million bpd of production as a lower cost source of oil production. This was a very unfavorable supply-demand imbalance that caused substantial downward pressure on dayrates. Unlike the prior cycle, today’s market is not burdened by a large speculative newbuild overhang, materially improving supply discipline.

The drillship market in 2025 was not strong but exhibited far better fundamentals and therefore dayrates did not come close to matching Pareto’s survey whereby their 60% of their clients expected dayrates between $200k-$250k. Since then, 7G drillship dayrates have ranged from $350k to $450k with a weighted average (by term) of ~$401k. Importantly, drillers have mostly maintained price discipline in 2025.

Pareto’s survey reflected excessive pessimism — a hurdle that has now been cleared. Since then, sentiment has improved although the global oil price markets remain fairly weak given concerns about supply in 2026. While all future contracts will reflect regional, project and rig specifics, dayrates are likely to stabilize in the current range waiting for utilization rates to firmly improve.

While 7G drillship dayrates have clearly declined from their most recent peak (as of announcement date) in the $480k-$490k range in mid-2024, they appear to have largely bottomed around the $400k level (average). Note that in deepwater floaters, a meaningful lag exists from negotiation to contract announcement that can span two to three quarters. While near-term Petrobras awards are unlikely to show pricing improvement as drillers prioritize utilization, equity markets remain forward-looking, with utilization expected to recover into 2H26 and 2027

Drillers expect utilization to improve, but meaningful dayrate upside requires firmer utilization and oil price stability to restore negotiating leverage. A return toward ~$500k/day is unlikely in 2026, though a plausible path exists for 7G drillships in 2027, contingent on multiple variables.

(1) Transocean 7G+ Drillship Contracting

Transocean’s 7G+ drillships Asgard, Conqueror and Proteus are key follows for early 2026, as their current contracts are scheduled to roll off. The primary distinction between 7G+ and standard 7G drillships is higher hookload capacity—1,400 short tons versus ~1,250—which enables greater drilling efficiency. Chevron currently operates Asgard and Conqueror and has only one deepwater rig contracted in the U.S. Gulf beyond 4Q26. Given Chevron’s public commentary on Permian maturation and its stated plans to drill 10–15 exploration wells in the Gulf of America, the IOC is likely to maintain its regional rig count, implying potential demand for additional drillships beyond 2026.

A key open question is whether Chevron prioritizes 7G+ capability or lower-cost contracting. Chevron has historically favored the highest-specification rigs in the U.S. Gulf, including the 8G Deepwater Titan at Anchor, which achieved first oil in 2025. The decision will likely hinge on whether Chevron extends its existing 7G+ units (Asgard and Conqueror) or adds standard 7G drillships at lower dayrates.

In April 2025, Noble signed two four-year contracts with Shell for Voyager and Venturer, including equipment upgrades that effectively reclassify both rigs as 7G+. Shell, historically the primary operator of Transocean’s 7G+ fleet since the mid-2010s, now appears to be shifting away from two Transocean units in favor of the upgraded Noble rigs. Shell is funding the upgrades and, in return, secured performance-linked contracts with approximately 20% of contract value contingent on meeting operational metrics. A key 2026 watch item is whether additional standard 7G drillships (e.g., Seadrill or Valaris units) are upgraded to 7G+.

(2) Standardize and Simplify: Deepwater's Cost Revolution

Capital efficiency in deepwater E&P has improved materially over the last decade. Unlike the prior cycle, when projects often underwent multiple, bespoke engineering phases, today’s developments emphasize simplified, repeatable designs that reduce engineering costs and shorten time to first oil, improving time-value-of-money on multi-billion-dollar investments. Industry focus on “standardize and simplify” is well illustrated by Shell’s Vito project, where costs were reduced by ~70% from the original design and over 80% of that design was replicated for the subsequent Whale development in the U.S. Gulf. Once floating production infrastructure is installed, incremental infill drilling further benefits from lower-cost brownfield capex.

(3) Seadrill remains the most likely consolidation target

In 4Q24, the upcoming year of 2025 was viewed to be weak with the first half of 2026 also expected to be soft. The market appears to have avoided persistent multiyear project delays thanks to progress in West Africa. Generally, soft market conditions create opportunities for consolidation where room exists for meaningful efficiency gains. While the deepwater drilling market has already successfully closed on consolidation, most IOCs continue to exhibit capital discipline where they are very cautious with capex spend (ie demand for offshore drilling rigs). While the expectation is for 7G drillship utilization rates to improve into 2026-2027, the negative carry costs while idle costs burden shareholder returns for drillers — effectively subsidizing capex flexibility and option value for their E&P customers. While this is typical for oilfield service companies, idle time on rigs contribute to pricing pressure on dayrates.

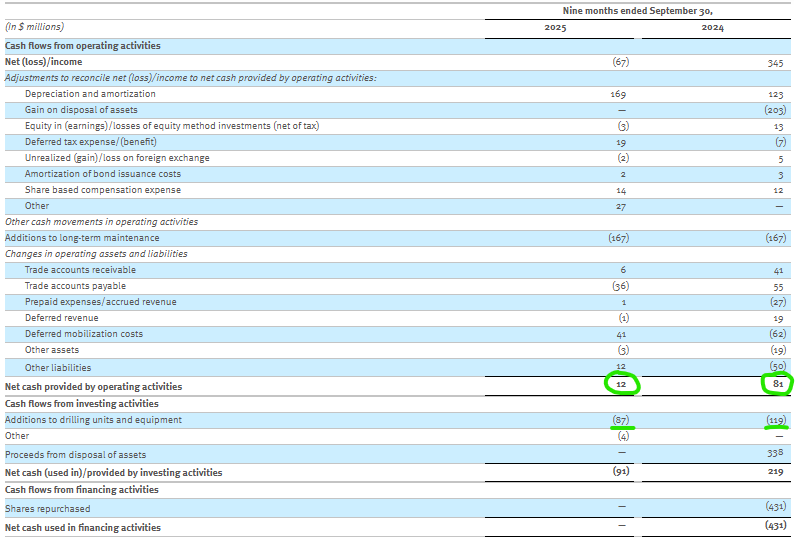

News sources, including Bloomberg, have noted Seadrill as a rumored candidate for consolidation. Seadrill has an active share repurchase plan but is not generating enough internally generated cash flows to use it without spending down its cash — prior repurchases were funded by the sale of three jackup rigs in 2024. As shown in Seadrill's 3Q25 cash flow statement, the driller has struggled to generate recurring cash flow for shareholder returns.

Seadrill’s cash flow has been hurt by legacy 7G contracts signed in 2021 that are only now rolling to higher dayrates, alongside recent start-up costs as rigs transition to new work. As noted in the cash flow statement, its operating cash flow generation remains insufficient to cover capex, notably including ~$76mm of SG&A incurred through the first nine months of 2025 (~$14mm of this was paid in shares), limiting Seadrill’s ability to self-fund shareholder returns without balance sheet deterioration. Noble realized ~$100mm of synergies from its Diamond acquisition, suggesting similar upside could exist in a Seadrill takeout by a larger player such as Transocean, Noble or Valaris. For Transocean, Seadrill’s low-leverage balance sheet would be deleveraging in a share-based deal and could accelerate a path toward recurring shareholder returns.

Complicating potential M&A, Seadrill has outstanding lawsuits. One with Eldorado Drilling and another with SFL where an appeal process is expected to commence in April 2026. Additionally, Seadrill is rumored to want to have a contract on its currently idle West Capella drillship to receive appropriate value for the asset. Capella is believed to be close to being awarded a contract in Malaysia with PTTEP with an announcement expected in coming weeks.

If Seadrill remains independent, the offshore drilling market still offers roll-up potential among sub-scale contractors with 1–3 rigs, which could benefit overall market structure. These smaller players are more vulnerable to idle time and thus more likely to bid aggressively for utilization, while larger drillers such as Transocean, Valaris, and Noble can better absorb idle periods due to broader, diversified fleets.

(4) “Scrap, Baby, Scrap”?

In 2025, Transocean, Valaris, and Noble collectively scrapped or retired at least 14 floating rigs. Notable retirements included Transocean’s Henry Goodrich, GSF Development Driller I, and several Discoverer-class units; Valaris’ DPS-3, DPS-5, and DPS-6; and Noble’s Pacific Scirocco, Pacific Meltem, and Globetrotter II.

While 14 retirements represent roughly ~10% of the global floater fleet (depending on definition), the market impact was limited. The majority of these rigs were cold-stacked, lower-specification units with minimal realistic prospects for reactivation. In practice, only three retirements were commercially relevant: Valaris’ DPS-5 and Noble’s Globetrotter II, both of which had drilled relatively recently, and Pacific Meltem, which—despite being cold-stacked—was a 7G drillship and therefore notable from a future capacity perspective.

Overall, while the headline number of retirements appears constructive, most removed capacity was low probability of re-entering the market, limiting the immediate tightening effect.

(5) Norway’s Offshore Strength Expected to Continue into 2026

The best offshore rig market of 2025 was the Norwegian Continental Shelf (“NCS”), as evidenced by Odfjell Drilling’s >60% equity return in 2025 despite Brent crude oil prices declining by $13/bbl in the year. The NCS is a supply-constrained market where eligible rigs must meet strict technical standards. Additionally, E&P capex in Norway is predominantly infrastructure-led, which is lower cost as it leverages existing infrastructure which supports the market’s resiliency.

The NCS is a mature oil and gas province, producing approximately 1.9 million bpd as of November 2025. NCS-eligible semisubmersibles operate under stringent regulatory standards—supporting higher costs—but benefit from a stable operating environment, extensive existing infrastructure, and predominantly brownfield development. E&P investment is further supported by Norway’s favorable tax regime, which incentivizes drilling and underpins long-term hydrocarbon supply to Europe.

(6) Greenfield Deepwater FID’s

Namibia: Following ExxonMobil’s success in Guyana, major discoveries by TotalEnergies and Shell in 2022 raised expectations that Namibia could follow a similar trajectory. However, Namibia is unlikely to replicate Guyana’s outcome—where capacity is expected to exceed 1.4 MMbpd by 2029—given higher development costs and later timing; reaching even half of Guyana’s production would be a favorable outcome.

A key 2025 development was Galp’s marketing of its Mopane discovery and the selection of TotalEnergies as a farm-in partner. Total acquired a 40% stake in Mopane, contributed a 10% interest in Venus, and agreed to carry 50% of Galp’s initial Mopane development costs. While the deal modestly tempers long-term deepwater floater upside—given disclosures that Mopane trails Venus by ~2–3 years—TotalEnergies appears closer to FID on Venus, discovered in 2022 versus Mopane in 2024.

Venus faces challenges, including low permeability, ~3,000 m water depth, and associated gas, while Mopane benefits from better reservoir quality and shallower water depth, partially offset by the cost impact of the carry structure. Venus FID remains pending and will hinge on fiscal stability and royalty certainty.

Greater clarity on Mopane is expected following appraisal drilling likely in 2026, likely beginning with appraising the Mopane-3 discovery in 2025 in a more oil-prone area of the field. Separately, Rhino Resources and Azule Energy have made three discoveries in PEL 85—including Capricornus-1X, one of the basin’s strongest exploration results to date—and, with appraisal likely in 2026, could deliver first oil ahead of Mopane, supported by their rapid execution track record at Angola’s Agogo project.

Indonesia: While Namibia draws headlines, arguably the strongest deepwater project is Eni–Petronas’ Kutei Basin gas development, anchored by Geng North and related discoveries. Backed by existing infrastructure and a self-funding JV, the project is expected to reach FID in 2026 with up to two multi-year drilling contracts—potentially including the 7G Deep Value Driller. With an existing LNG plant and short shipping distances to Asian markets, Kutei is a rich-gas project likely to reach market faster and with better economics than Namibia.

Mozambique: After the security situation has stabilized in key deepwater LNG projects, TotalEnergies and its partners lifted force majeure on Mozambique LNG in October 2025; while the region remains sensitive, Exxon and TotalEnergies appear to be progressing projects following Eni’s FID on Coral North FLNG.

Excellent. Thanks for sharing this research. Much appreciated.

Thanks for writing such a concise, highly-informative article!