Borr/Paratus Jackup M&A and Brazilian Deepwater Market Update

Borr's Mexican jackup consolidation, Paratus's PLSV residual, what regional driller contracts reveal about Brazilian deepwater dayrate expectations ahead of the Buzios tender

The following note covers Borr Drilling's acquisition of Paratus Energy's Mexican jackup fleet, Paratus’ remaining PLSV fleet, and key Brazilian deepwater market developments from regional drillers Constellation and Foresea to Buzios productivity enhancements.

Borr Drilling acquires five Mexican jackups from Paratus Energy (Fontis Finance) for $287mm (excluding working capital), with a $237mm seller's note to a newly formed JV introducing incremental credit complexity for Paratus bondholders

Following the jackup sale, Paratus’ remaining asset is its 50% stake in the Seagems PLSV JV, with a strong contract book through 2027–2028 in an attractive Brazilian market

Constellation Oil Services' earnings call flagged two near-term Brazilian catalysts: conclusion of Petrobras' Renecon efficiency program in early April and pending Buzios multi-rig tender results. Also Foresea’s new 6G ODN I contract

Before diving in, the Middle East conflict has removed an estimated 7–10 million bpd from global oil supply, an extraordinary volume that excludes Qatari LNG disruption. For deepwater, the impacts are not immediate given long-cycle capex lead times, but the energy security implications are constructive for the market over the medium term. The recent Brazilian contract awards discussed below reflect 2025 market conditions — these tenders are roughly nine months old — and while dayrates are soft, they should be read in that context. Lower crude prices through 2025 pressured oil major cash flows and contributed to project delays, constraining rig demand which is a headwind that is abating with Brent near $100/bbl, which should support capital budget expansion and incremental drilling activity in 2027.

On March 23, 2026, Borr announced the acquisition of five jackup rigs in Mexico from Fontis Finance (Paratus Energy) for $287mm, inclusive of over $100mm in associated receivables, for a total transaction value of approximately $400mm. Paratus will receive $148–163mm in cash and a $237mm seller's note as consideration. The seller’s note is essentially secured bridge financing to BC Ventures Limited, a newly formed 50/50 JV between Borr and its Mexican well construction partner, carrying a 2.5-year maturity with a step-up coupon: 10% in year one, 12% in months 13–18, and 14% thereafter. Borr already has a presence in Mexico and acquiring 5 competing jackups in the region will be positive for its pricing power in the region.

Borr was a logical acquirer following Paratus's public signaling of its intent to divest its jackup fleet, particularly given Borr's stated plans to deploy proceeds from its $200mm equity offering in early July. In August 2025, prior analysis noted potential for a Borr/Paratus jackup transaction with an estimated $280-$300mm price range, making the $287mm headline figure (excluding working capital) within the expected range. However, the consideration structure is less clean than an all-cash deal. The $237mm seller's note from a newly formed JV with a 2.5-year maturity is clearly less ideal than cash, although BC Ventures is incentivized to refinance given the step-up coupon.

Given BC Ventures' JV structure, how the entity refinances this note will be worth watching — particularly whether it taps the USD bond market or finances separately against the new collateral pool. A standalone structure would likely carry an elevated coupon given the limited collateral and heavy Mexico concentration (for now). Separately, a $150mm seller's note from Noble's January 2026 rig acquisition also remains outstanding, secured by five rigs and subject to its own eventual refinancing but does not have a JV structure.

Paratus has designated the transaction a 'Material Asset Sale' under its 2029 bond indenture, requiring bondholder amendment to permit a seller's note in lieu of full cash proceeds — a negotiation worth monitoring given the credit implications. Strictly from a credit perspective (not bond pricing and early redemption), if I’m a Paratus bondholder I want to be paid down in cash from an asset sale, not a seller’s note from a newly created JV with a non-IG credit profile. The seller's note is secured by the five rigs, but the obligor is BC Ventures, a newly formed JV with a credit profile distinct from Borr consolidated. On balance, both JV partners contributed $25mm in cash equity, reflecting meaningful alignment, and the Mexican jackup market appears positioned for cyclical recovery after recent softness. With two rigs currently idle, a refinancing of the seller's note will likely follow recontracting.

The current war in the Middle East has had an impact on the shallow water jackup market, which accounts for 35-40% of global demand. Borr enters 2H26 with 48% of its fleet open at a $139k average dayrate. Diversification across the GoM, West Africa, SE Asia and Europe should support utilization at current oil prices, though dayrates may depend on conflict duration and whether Mid East rigs are ultimately relocated, which is not currently expected to a material extent.

The Middle East conflict should support jackup demand in Mexico, and Borr's consolidation of five additional rigs in the region strengthens its pricing power, a key strategic rationale for the acquisition in an elevated oil price environment. While short-cycle jackup demand should improve in 2026, longer-term Mexico’s deepwater market is looking intriguing…

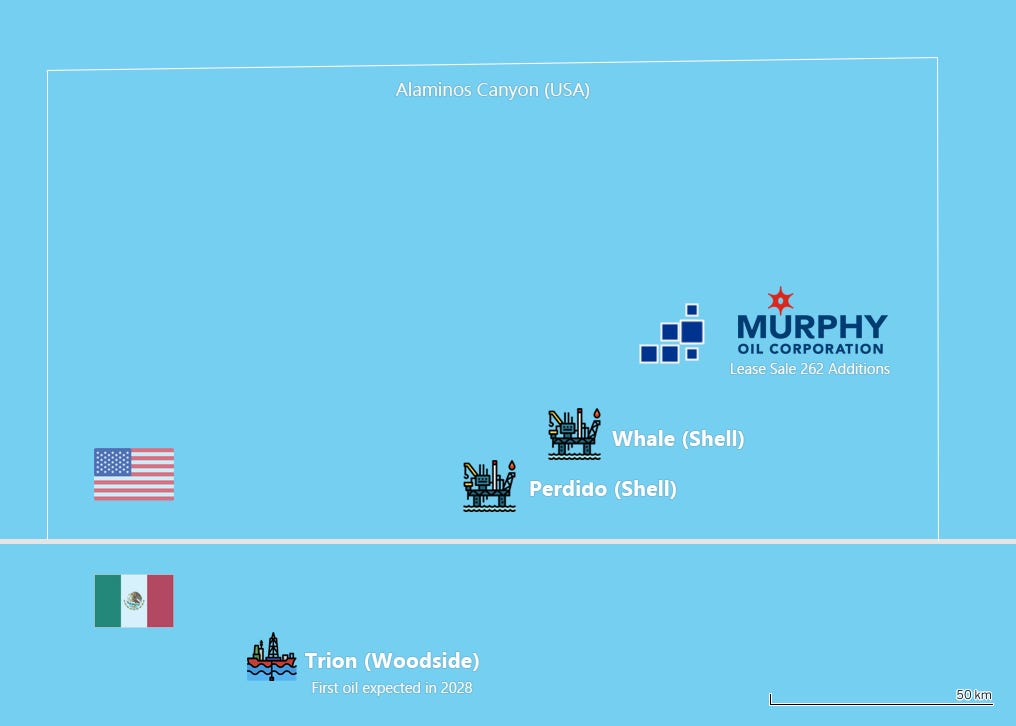

While Mexico's Gulf production is predominantly shallow, deepwater potential is emerging — Shell's Perdido and Whale developments in Alaminos Canyon and Transocean's Deepwater Thalassa, currently drilling Woodside's Trion project on the Mexican side, sit in close proximity and signal growing ultra-deepwater activity along the Perdido fold belt on both sides of the maritime boundary.

Woodside operates Trion at 60% alongside PEMEX at 40%. Strong project performance could validate the Perdido fold belt's extension into Mexican waters as a credible exploration frontier, potentially commanding a growing share of PEMEX's deepwater budget. Given the long-cycle nature of deepwater capex, potential projects beyond Trion are unlikely to compete meaningfully against PEMEX short-cycle jackup demand over the next 12 months. However, the region’s material prospectivity makes it worth watching toward decade-end.

Brazilian Deepwater Offshore Market

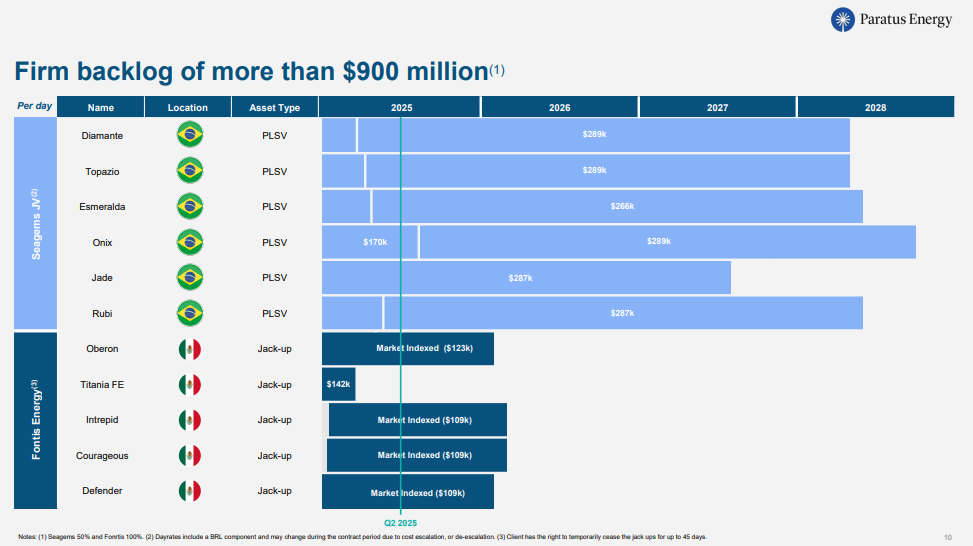

Turning to the Brazilian market — following the jackup divestiture, Paratus' remaining assets are through its 50% interest in the Seagems JV, which owns six PLSVs that install subsea pipelines connecting wellheads to FPSOs. This is a distinct vessel class from offshore supply vessels (Tidewater focus), where Subsea7, DOF, and TechnipFMC as the primary competitors. Paratus's PLSV fleet carries a strong contract book extending into 2027–2028, with exposure concentrated in Brazilian deepwater E&P capex.

The PLSVs are arguably the stronger assets, and a pure-play PLSV strategy appears to be Paratus' goal. Exposure to Brazil's Santos and Campos basins is an attractive position given pre-salt field productivity, though the outlook beyond the Buzios ramp-up in 2027 is less certain. Petrobras capex toward decade-end and into the 2030s remains an open question, as the next growth legs in Brazil are underexplored with a wide range of potential outcomes.

The Brazilian deepwater floater market came into sharper focus Tuesday when Constellation Oil Services (seven owned rigs, including one 7G drillship) held its earnings call, flagging two near-term catalysts: Petrobras' Renecon capital efficiency program is expected to conclude in early April, likely through blend-and-extend agreements on contracted rigs, with the long-awaited Buzios multi-rig, multi-year tender results to follow. Constellation announced a 1,042-day extension on an undisclosed rig at an implied dayrate of ~$255k ($266mm backlog), believed to be a lower-tier unit rather than the 7G Brava Star. Notably, the extension carries no associated capex or downtime.

Also on Wednesday, regional driller Foresea announced a 1,443-day contract for the 6G drillship ODN I with Petrobras on the Mero tender, commencing early 2027 at $280–300k per day (depending on additional services), with an early termination option at 1,078 days. The rate reflects both the lower operating cost structure of regional drillers, lower utilization outlook in 2025 when tenders began and the depth of competition in the Brazilian market, where Petrobras has its choice among the major international contractors (Transocean/Valaris, Seadrill and Noble) alongside several regional players, most notably including Constellation and Foresea.

Petrobras benefits from a group of regional drillers with low to mid-level spec deepwater rigs that value utilization over dayrate, as emphasized by Constellation’s conference call on Tuesday where they discussed the ~$255k dayrate (no capex, no downtime) dayrate on a likely 6G semisub.

However, a mid-$200k contract through 2029 is unfavorable dayrate duration. In the Paratus graphic above, all six of their PLSV’s are contracted at dayrates above $255k despite arguably costing materially less to build than Constellation’s semisubs. If the unnamed rig is Gold Star, with its current contract expiring in 1Q26, near-term idle exposure ahead of major tender commencements in 1Q27 likely weighed on the blended dayrate. While Constellation has more size than its regional peers, the smaller drillers seem to value utilization over dayrate. These are arguably subsidizing Petrobras’ E&P capex returns but this is a market dominated by one player which has a variety of drilling contractor choices with the regionals in the country.

A key rate watch in the Buzios tender is Brava Star, Constellation's only 7G drillship. The rig is expected to be included in Petrobras' Buzios tender for up to four rigs beginning 1H 2027 on approximately 3–4 year terms, a process that has been outstanding since at least summer 2025. The delay is attributable in part to Petrobras' efficiency program, and the eventual results will likely reflect the weaker conditions that prevailed when the tender was live. Regional drillers bidding aggressively for utilization are expected to suppress regional dayrates into the mid-to-upper $300k range. Seadrill’s 7G West Carina is also a potential drillship to be included in the Buzios tender, although has also been marketed internationally. These rates should not be read as indicative of the broader global 7G market, which is meaningfully healthier — particularly post Transocean-Valaris merger — but Brazil is a distinct dynamic where Petrobras commands a competitive, multi-operator market and effectively extracts the benefit of that competition through lower contracted dayrates.

The Buzios tender is a significant market event and likely represents a cyclical trough in deepwater dayrates given the extended award lag, considering it began when floater utilization rates were low. The field's importance extends well beyond contracting — by 2027, three FPSOs with nameplate capacity of 225k bpd each are scheduled to come online, with Petrobras recently signaling efforts to push that figure toward 270k bpd per unit. If any deepwater field can deliver that kind of productivity enhancement at scale, Buzios is it.

Always appreciate your analysis. Thank you Tommy.