Borr: 10 Thoughts on the Bond Refinancing

An alternative pre-sale report

Borr launched a $1.6 billion senior secured notes offering this week. What follows are ten quick thoughts on the credit, published within 24 hours of announcement.

Borr was built on an opportunistic thesis: acquire high-specification jackups at discounts to newbuild cost using creative financing. The foundational deals were completed in 2017 — 15 jackups from Transocean for $1.35 billion and nine undelivered newbuilds from PPL Shipyard for $1.3 billion. These acquisitions and some smaller deals built Borr, and the company has subsequently made other acquisitions in 2025 which include 5 rigs from Noble Corp and another 5 rigs from Paratus Energy Services (Fontis).

Borr has utilized debt to support its asset-heavy balance sheet. At 1Q26 LTM EBITDA of $462.5MM, Borr is ~4.5x secured net leverage (5.1x total). This will turn off some credit investors especially considering it’s an offshore driller, although it’s a strong asset base with an earning potential exceeding its trailing performance.

Borr announced on Tuesday it was in the USD high yield market to raise $1.6B of new senior secured notes due 2032 and 2034 with the proceeds to refinance its $1.13B of notes maturing in 2028 and up to $447mm of its ~$775mm of 2030 maturity. This follows April’s $300mm convertible note issuance with proceeds to repurchase its $240mm of convertible notes due in 2028.

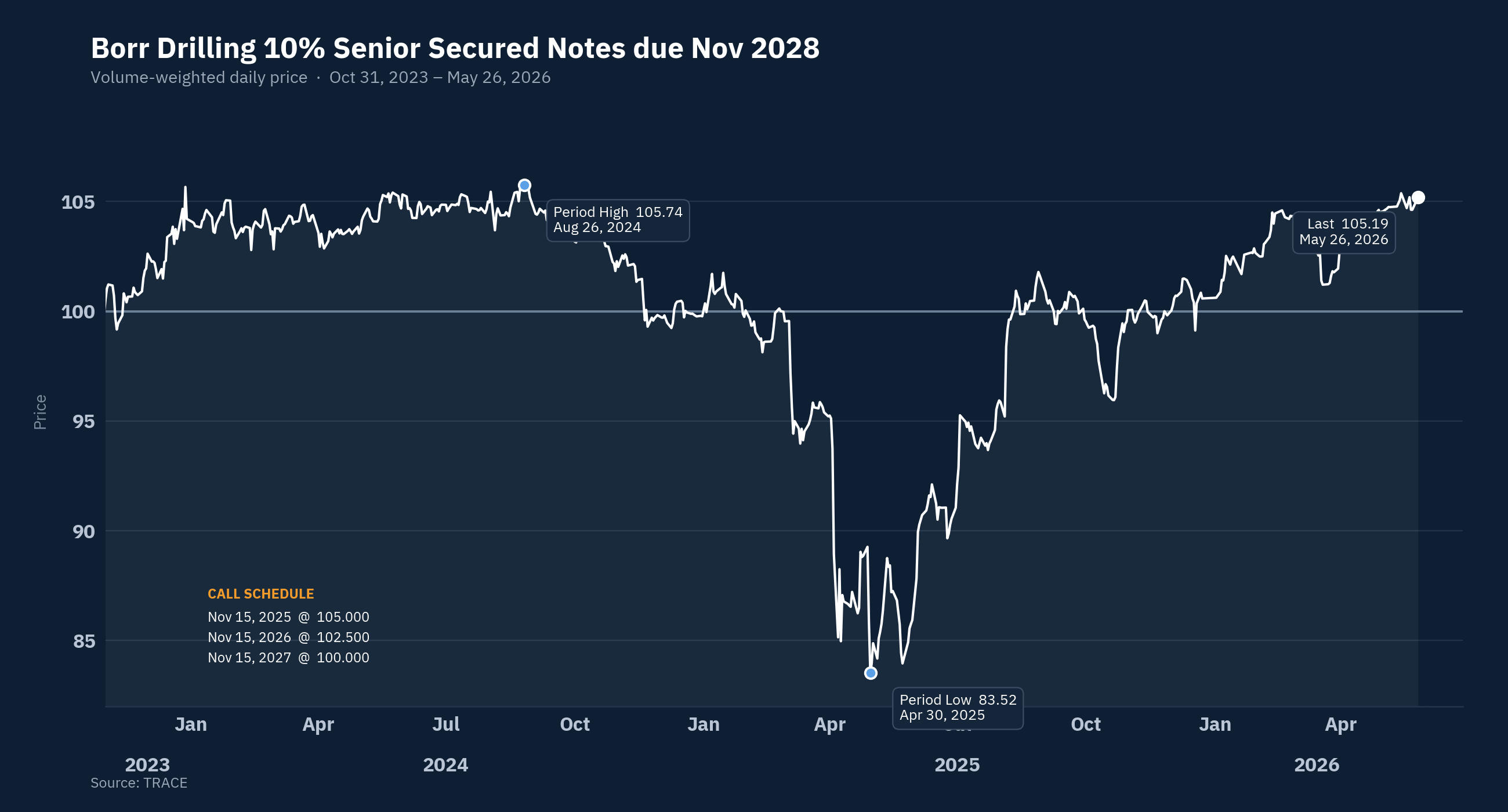

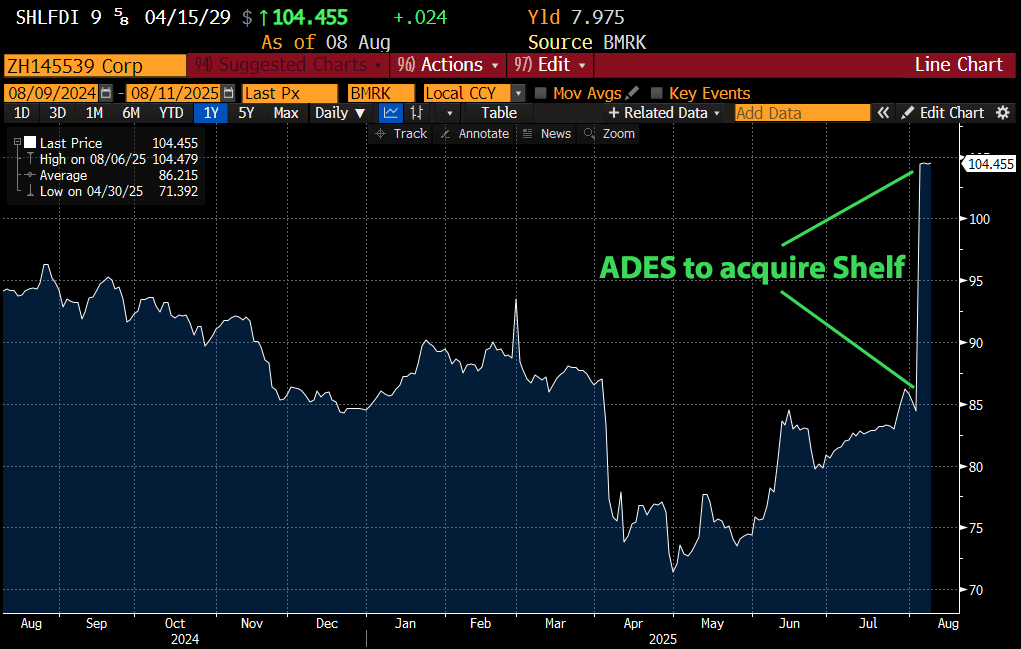

After “Liberation Day” market weakness in 2Q 2025, Borr’s senior secured bonds traded at credit spreads between 1,100 and 1,400 bps which also had to do with weak oil prices, concerns about the jackup market and meaningful ‘white space’ on its 2026 contract book at the time. As noted in the chart below, Borr’s 10% coupon 2028s have rallied all the way back to 105 and the company is using the opportunity to extend its maturities to 2032 and 2034, subject to market execution. The proposed transaction will meaningfully improve Borr’s maturity profile.

Below are ten thoughts worth considering about Borr and the current transaction:

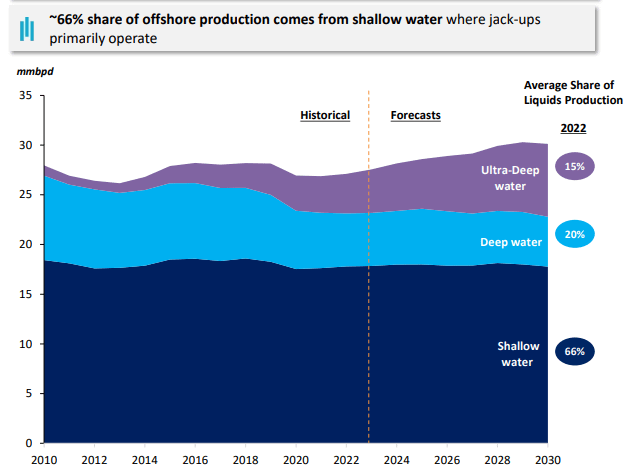

(1) Borr’s fleet is 100% jackup rigs designed to work in shallow water. Shallow water E&P investment tends to be lower cost and shorter-cycle when compared to deepwater. Accordingly, jackups have historically been more stable through cycles as they performed better than deepwater floaters in the 2015-2021 downturn, however jackup credit performance was weaker in the more recent 1H25 bear market.

Shallow water accounts for the majority of offshore production, but the chart above notes a stronger growth trajectory for deepwater — driven by Brazil, Guyana, and a growing discovery portfolio that is claiming a larger share of oil major and NOC capex. Deepwater project costs have fallen as designs standardize, though shallow-water jackup barrels remain lower-cost and shorter-cycle.

(2) I will forever be cautious of investing in New Issue oil credits at $100/bbl after living through 2015-2016. Some key items to consider on Borr include its credit underperformance versus broader offshore market in 2Q25, reflecting two headwinds: jackup market weakness driven by Aramco's outsized demand swings, and the company entering 2025 with only 23% contract coverage for the 2026 calendar year.

Regarding contract coverage, a major difference between jackups and deepwater floaters is jackups are shorter-cycle and often have shorter contracting cycles. Borr has improved contract coverage for 2026 to 71% total with potential to improve through the end of the year. A reflection of fleet quality, the dayrates have been better than feared a year ago and have been in the $130k-$140k range. Borr will need to improve utilization in the future, and part of this will rely upon the market in Mexico.

Mexico is a key market for Borr, and upon closing the Paratus/Fontis acquisition in 3Q26, Borr will have 8–11 jackups in the region (it can move rigs if needed). Mexican oil production has underperformed its targets, creating a longer-term case for increased drilling activity. However, Mexico was a meaningful credit overhang in 1H25 — PEMEX fell behind on payments, forcing Borr into a factoring arrangement to monetize receivables at a discount. The market remained soft in 2025–2026, though the Paratus fleet acquisition should improve Borr's regional pricing power, and any recovery in Mexican production ambitions represents upside to EBITDA.

Importantly, Borr issued equity around $2/share in the summer of 2025. While it was an expensive capital raise, the willingness to do so was credit friendly and helped support the acquisition of jackup rigs with potential for EBITDA growth.

(3) In recent years, the shallow water jackup market has been driven by Saudi Aramco. When Brent exceeded $100/bbl in early 2022, Saudi Aramco tendered aggressively for jackup rigs to support a capacity expansion from 12 to 13 million bpd — growing its shallow-water fleet from the low 50s to ~90 rigs, or roughly an incremental amount equal to 9–10% of global active supply. Combined with rising demand elsewhere, the program drove jackup dayrates from sub-$100K to the upper $100Ks by late 2023. However, in 1H 2024, weaker oil prices prompted Saudi Arabia's Energy Minister to freeze capacity targets at 12 million bpd, effectively reversing that incremental demand. Aramco subsequently announced multiple rig suspension rounds, unwinding nearly all demand growth tied to the expansion program in a short time period.

Prior to the escalation of hostilities in the Middle East, Saudi Aramco had been showing signs of re-engaging the jackup market — a constructive backdrop for contractors. While the current war clouds the market in the Middle East (35-40% of global jackup demand), the shallow water production will be an important part of the puzzle for sustaining Saudi Arabia’s production capacity as its legacy onshore fields mature. However, the timing of this demand is hard to pinpoint given the fluid geopolitical situation.

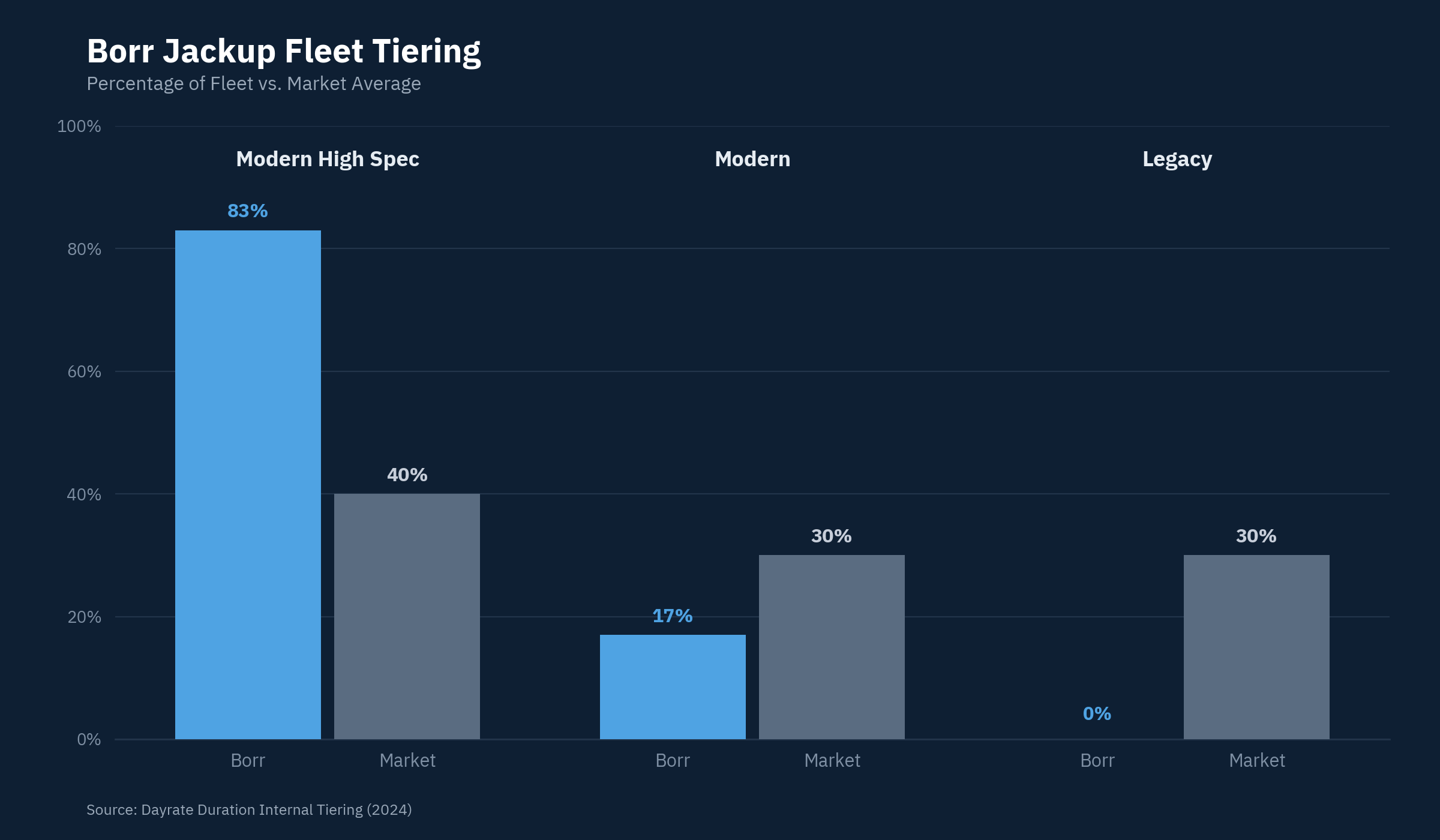

(4) Borr built an industry-leading fleet by acquiring high-specification jackups at discounts to newbuild cost. The jackup industry includes a meaningful amount of older rigs, which have their purpose, although Borr’s rigs are more modern and accordingly should generate above average dayrates and operate at above industry utilization rates on a through-the-cycle basis. As older rigs are gradually rationalized, Borr’s younger fleet should benefit.

The fleet tiering chart above was completed in early 2024. Use it as directional context rather than a precise ranking, but it illustrates where Borr sits relative to the broader market.

(5) While it costs $250-$300mm to order and build a new jackup rig, in offshore drilling you should not rely upon newbuild costs as any sort of reliable valuation metric. It is an easy reference point to keep in the back of your mind but when managing downside scenarios in credit, newbuild costs have limited relevance — asset transactions and dayrate-implied valuations are more instructive.

(6) Dayrates are a stronger explanatory variable in valuation exercises. Borr does not disclose individual contract dayrates, however by using the company's quarterly contract coverage and average backlog dayrate disclosures, we can back into the implied rate on new additions each quarter by isolating the marginal change in both coverage percentage and blended average dayrate. While not perfect methodology, it implies recent quarters’ dayrate additions have been in the $132-$144k range. Borr’s new presentation notes “leading edge dayrates approaching $170k”, but this is one specific market (West Africa) and is a misleading data point.

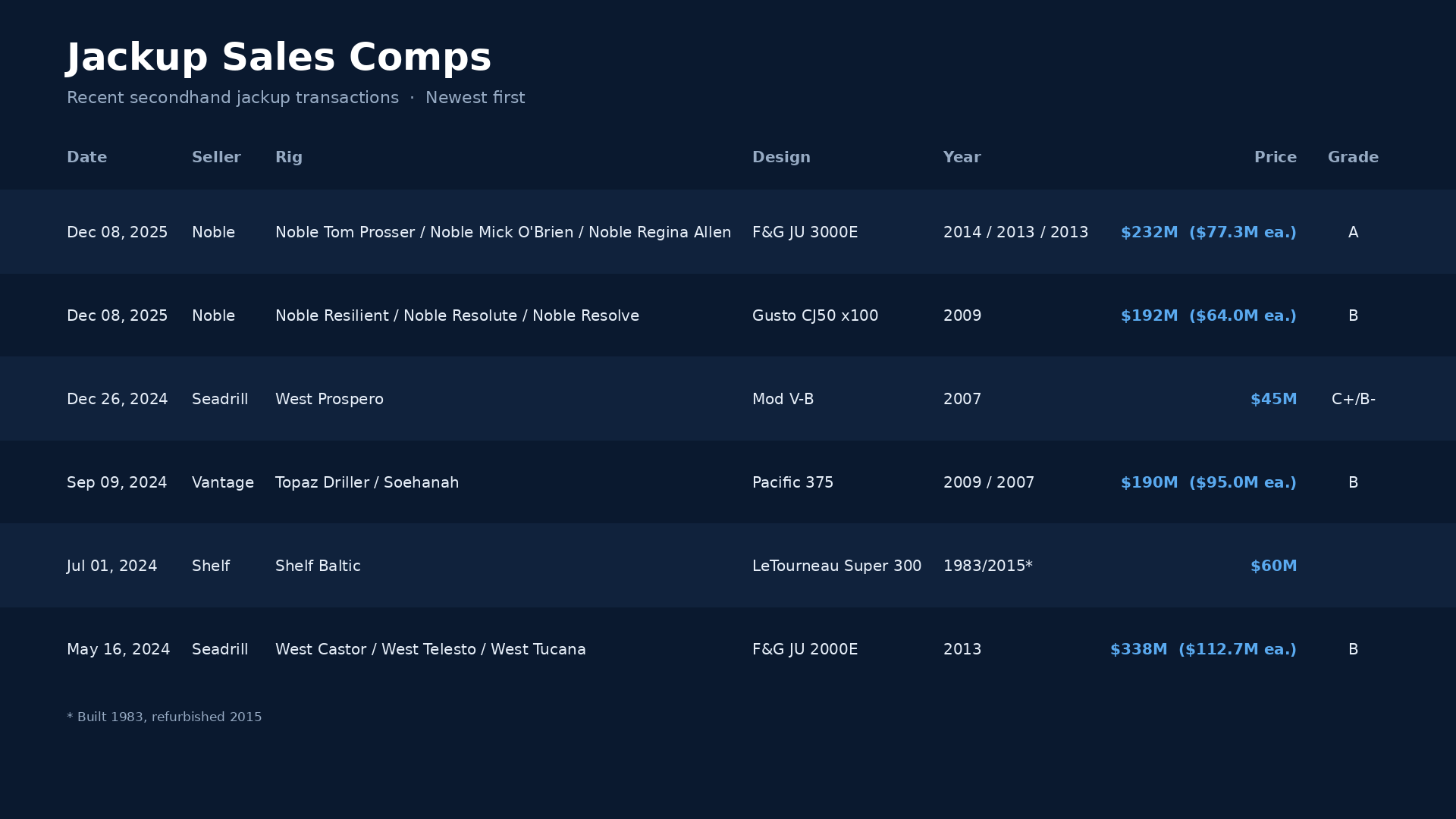

(7) The chart below shows various jackup sales transactions as reference points. The Seadrill sale of West Castor, Telesto and Tucana was executed before the full scope of Aramco's suspension program was known, and accordingly reflected stronger market conditions. Subsequent transactions have priced softer, but together the comps provide a useful range of jackup asset values across the cycle.

When considering Borr’s estimated enterprise value, consider that Borr has a $200mm super senior RCF that will take priority to the senior secured bonds in any potential restructuring in a downside scenario.

(8) In August 2025, Saudi Arabian driller ADES announced its all-cash acquisition of Shelf Drilling for approximately $1.7B enterprise value. The ADES acquisition of Shelf was somewhat surprising given Shelf’s high yield bonds were trading in distress at the time, but it was a constructive datapoint for the sector — validating demand for older, lower-specification assets and demonstrating appetite for consolidation in an otherwise more fragmented jackup market.

(9) Roughly one-quarter of the global jackup fleet is over 25 years old, and the industry broadly expects supply rationalization in the coming years. While some older, less efficient units will inevitably retire, jackups have historically proven fairly durable — refurbishment can meaningfully extend asset life, as Shelf's fleet demonstrated before ADES acquired it at a price that surprised many who had written a portion of its fleet as rationalization candidates. Given Borr’s younger fleet, industry fleet rationalization will benefit Borr over the next 5-10 years although the pace may require patience.

(10) Borr's elevated leverage comes with one bondholder-friendly feature: meaningful mandatory amortization. The 2028 notes require $101 million in annual principal repayments at par. While a drag on returns when buying the bonds above par, or investors buying in the 80s or 90s (such as in 2025), that creates an accretive dynamic — each amortization payment returns capital at par, effectively accelerating recovery of the purchase price discount. Of course, this assumes the borrower has the liquidity to make those payments and why diligent credit work matters. While the 2028 and 2030 notes are being refinanced away, required amortization is likely to remain on the new notes.

I still find it notable that their newest built rig, Var, continues to remain warm stacked since a Nov 2024 delivery. Why no analyst ever asks about it on the calls? Presumably they're tendering it at higher day rates on longer duration contracts ... but 18 months of no revenue! What does that say about the high spec jackup market?