10 Thoughts on the Transocean-Valaris Merger

A positive industry development in various respects.

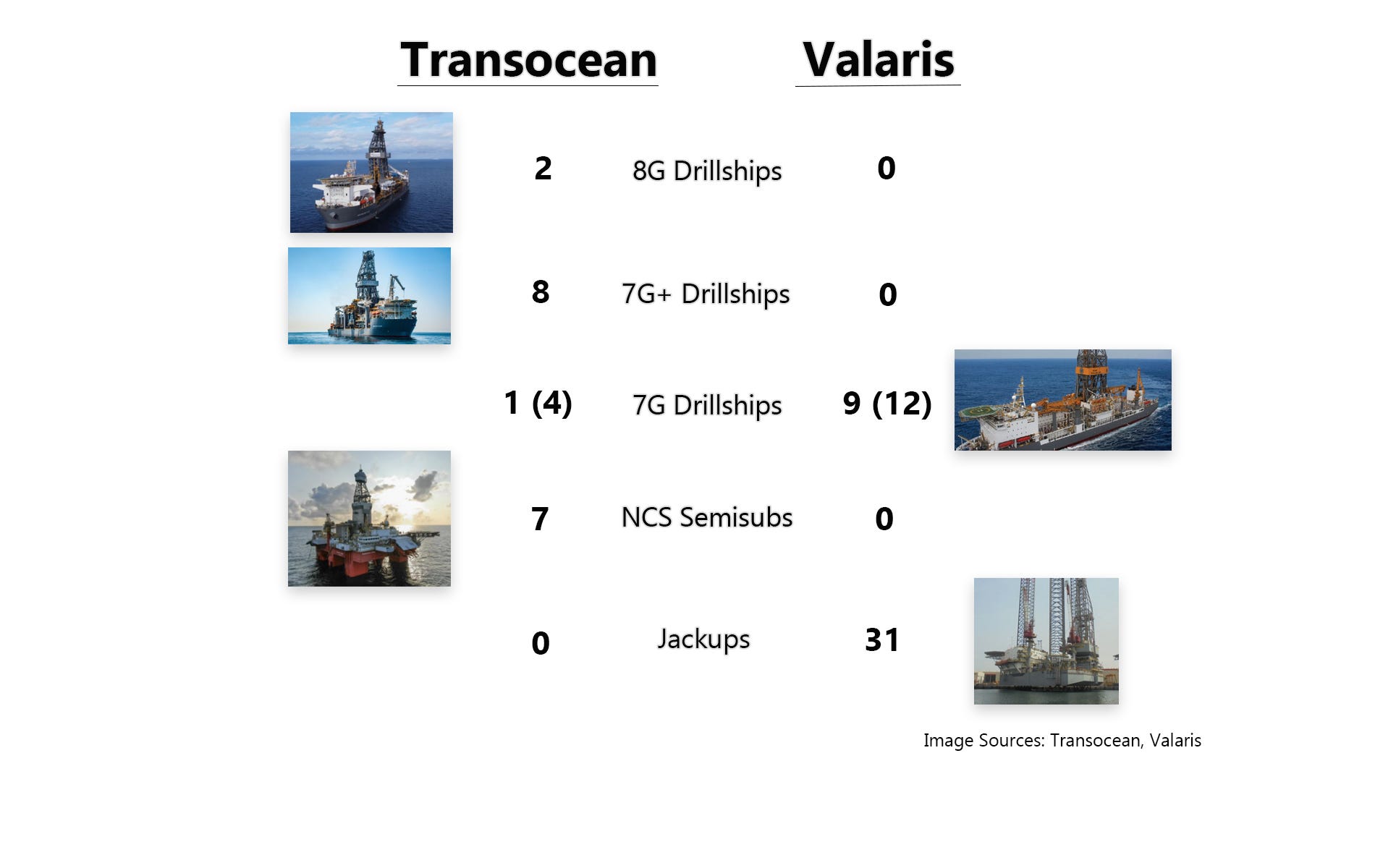

Monday morning, Transocean announced a $5.8 billion all-stock acquisition of Valaris, creating a globally diversified offshore drilling contractor. The combined fleet would include 24 seventh-generation drillships (~42% of global supply, including six cold-stacked), plus semisubmersibles and jackups.

The all-stock structure is materially deleveraging, pulling shareholder returns significantly closer for RIG equity holders

A key feature of the combination at closing is Transocean would have control of all six of the industry’s coldstacked 7G drillships. This is positive for the market structure and dayrate trajectory

Efficiency gains via ~$200mm of cost synergies, as well as improved industry pricing discipline

Transocean says it intends to keep Valaris’ jackup fleet, although could provide option value in the future for potential shareholder returns or deleveraging

In late September 2025, Transocean raised $421 million (net of fees) through an equity offering, using the proceeds to pay down debt after its stock price had appreciated significantly. As a natural consolidator given its scale, Transocean likely recognized that using shares as acquisition currency for M&A is far more capital-efficient than issuing equity for cash after recent share price strength. The Valaris merger achieves three objectives simultaneously: deleveraging (acquiring Valaris' underleveraged balance sheet), capturing $200 million in annual cost synergies and consolidating pricing power.

(1) Transocean is the industry’s most disciplined contract driller, earning premium dayrates through fleet quality and marketing discipline. Valaris, by contrast, often accepts weaker economics to maximize utilization—the recent DS-8 contract with Shell in Brazil at ~$375k exemplifies this, pricing a 7G drillship well below the >$400k threshold it should command even in softer markets. Valaris' post-bankruptcy capital structure enables this aggressive pricing, but consolidating their fleet under Transocean's commercial discipline should reduce competitive undercutting and support stronger dayrates industrywide, benefiting Noble and Seadrill as well.

(2) Transocean management stated on its call today: ‘We know our debt level negatively impacts our equity value.’ Offshore drillers operate like equipment lessors or financial entities—equity value depends on earning higher returns on long-lived rig assets than the cost of debt financing. Transocean owns industry-leading assets generating industry-leading dayrates, but due to its leveraged balance sheet, its creditors demand debt terms that consume most of its free cash flow, arguably making bonds more attractive than equity to various institutional investors. The proposed Valaris merger is the biggest swing Transocean can take to address this for its equity investors. By acquiring Valaris’ underleveraged balance sheet alongside 12 seventh-generation drillships and 31 jackups, Transocean’s leverage immediately reduces upon closing with net leverage gradually reducing to ~2x by year-end 2027—well below the previously communicated 3.5x threshold required to enable dividends and buybacks. This is a big step toward generating value for equity investors.

(3) Why would Valaris shareholders want RIG shares? They gain exposure to the industry’s premier fleet without expensive capital outlays. The deal delivers two 8G drillships and seven NCS-qualified semisubs—high-value segments VAL does not currently participate in. Noble just announced plans to spend ~$160mm upgrading GreatWhite for NCS access; VAL shareholders get that market exposure immediately. They also acquire RIG’s ‘7G+’ drillships, which while less differentiated versus VAL’s 7G fleet than the 8Gs or harsh-environment semisubs, still add fleet depth without diluting economics through upgrade capex such as Noble accepted in 1Q25 via contracts with Shell.

While Transocean lacks an existing shareholder return program, Valaris recent track record is underwhelming—just $75mm in buybacks during 2025, funded by an asset sale. An all-stock merger accelerates the timeline to shareholder returns for Transocean given the deal’s deleveraging nature.

(4) Odfjell Drilling trades at >$550mm per rig, the industry’s highest valuation primarily due to its positive dividend growth story. The NCS operator deleveraged from >3x Debt/EBITDA in 2022 to ~2.5x by 3Q23 through EBITDA growth and debt reduction, then initiated dividends that have grown steadily while its leverage has reduced to below 2.0x.

Transocean is tracking a similar trajectory to Odfjell, though a few years behind. RIG has deleveraged through contracted cash flows and the $421mm equity raise in 3Q25. The all-stock Valaris acquisition accelerates this path, potentially reaching ~2x net leverage by year-end 2027—a level that clearly supports shareholder returns at the combined company’s scale.

(5) The merger's most strategically interesting element may be control of three cold-stacked 7G drillships: DS-13, DS-14 and DS-11. Valaris faced criticism for premature rig reactivations years ago—rational from a cash flow optimization perspective but market-negative, as early supply additions capped dayrate recovery before utilization tightened sufficiently.

Transocean has demonstrated greater supply discipline and would control all six of the industry’s coldstacked 7G drillships. The DS-13 and DS-14 are rumored to be involved in current marketing efforts and it seemed as though Valaris was eager to reactive DS-11 which could have suppressed market dayrates. Critically, Transocean is more likely to only reactivate when dayrates justify the capital investment—Valaris has publicly stated the same but actions often speak louder than words. This consolidation benefit alleviates investor concerns about sidelined 7G capacity flooding the market prematurely, particularly after TPAO’s acquisition of previously coldstacked 7G drillships Dorado and Draco in July 2025.

(6) The industry is closer to avoiding inefficient capital upgrade cycle. Noble’s recent floater upgrades (GreatWhite, Voyager, Venturer) highlighted an industry concern of mine: Valaris pursuing similar capex upgrades to access premium markets. These upgrades divert cash flows from shareholders to equipment vendors, funded through either direct capex, reduced dayrates or operator options post-initial contract. Transocean is much less likely to invest in substantial upgrades to Valaris’ 7G drillships—they’re already capable for Africa, East Med and Brazil work. This removes upgrade risk for former VAL shareholders who faced potential capital diversion to keep up with competitors, which was a meaningful concern in a less consolidated industry.

(7) Valaris operates 31 jackups across Saudi Arabia, UK North Sea and other markets. While Transocean currently has a deepwater focus—where exploration discoveries arguably drive stronger growth trajectories (my opinion)—management emphasized on the call that it values the jackup fleet. The jackup fleet diversifies cash flows across different markets and customer bases than deepwater, and historically is less cyclical. The jackup fleet may provide eventual strategic optionality: potential asset sales could fund further deleveraging and/or share repurchases.

As a part of the acquired jackup fleet, Valaris has ~$1B in potential newbuild obligations through 2030 via its ARO JV with Saudi Aramco. However, not all may be required, and the JV has historically funded deliveries through available cash and third-party financing rather than parent equity. Completed newbuilds come with multiyear contracts in a strategically important market. The ARO JV is a concern of mine on this transaction but shallow water market in Saudi Arabia is improving in recent months.

(8) The merger is subject to global regulatory approval, but regulatory risk does not appear to be substantial per Transocean commentary today. On drillships, Transocean has a different class of premium “7G+” drillships most heavily demanded in the US Gulf, while Valaris’ 7G drillship fleet tends to have more exposure to Africa, the East Med and Brazil. Additionally, Valaris’ semisubmersible fleet generally targets different markets than Transocean’s, and Valaris’ 31 jackup rigs represent an entirely new asset class for Transocean.

(9) Could Transocean achieve investment grade ratings again? Unlikely! The rating agencies are likely to keep offshore drillers in the high-yield bucket for years, penalizing the industry’s historical volatility regardless of absolute leverage levels. Even if Transocean could reach IG by maintaining sub-1.5x leverage, shareholders won’t support the conservative capital allocation required. Instead, equity holders will demand dividends and buybacks funded by robust free cash flow—capex needs are minimal with no newbuild cycle on the horizon—making the pursuit of IG ratings both unlikely and strategically misaligned.

(10) The merger is expected to generate $200 million in cost synergies, which unfortunately means headcount reductions—though this industry has meaningful room for efficiency gains. Many institutional investors avoid offshore drilling because these companies consistently struggle to earn their true cost of capital: the industry needs ~$600k dayrates to generate adequate true returns, yet recent drillship contracts are pricing around $400k. Long-term deepwater demand fundamentals remain constructive, but this is a volatile industry. Consolidation of two large players like Transocean and Valaris is a key step in the right direction of improving capital returns from the value they provide to E&P clients and eventually enabling consistent shareholder returns to the combined entity.

There was quite a lot of commentary on X this morning regarding this merger, most of the sources lacked your history and depth of knowledge in this specialized thinly covered sector. Your positive analysis holds a great deal of creditability, I can rest easy, thanks.

Many thanks for sharing your research and ideas - very helpful.